Choosing among the leading Flexible Countries for SPV tokenization is not merely a company incorporation exercise. The chosen location can affect the token’s legal status, available investors, licensing requirements, banking relationships, custody arrangements, taxation, reporting, and secondary transfers.

A jurisdiction may offer flexible company formation but impose strict securities rules. Another location may provide a clear tokenized securities framework while requiring regulated intermediaries for issuance, management, custody, promotion, or trading.

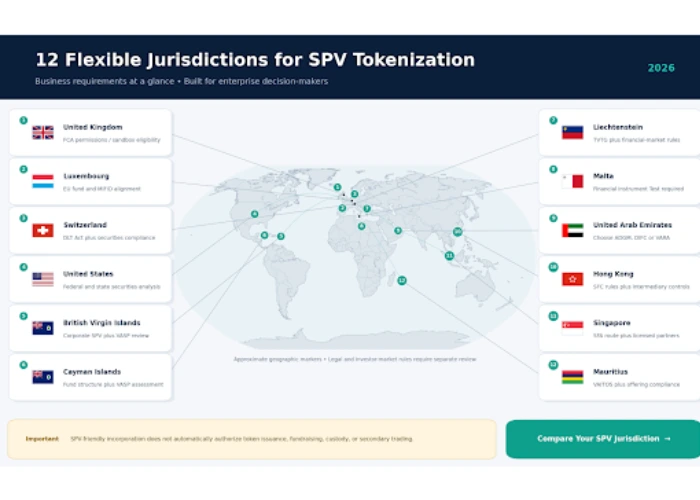

This guide evaluates 12 tokenization-friendly jurisdictions according to their practical value for real estate, investment funds, private equity, private credit, bonds, commodities, company shares, and other real-world assets.

What Is SPV Tokenization?

A Special Purpose Vehicle, or SPV, is a separate legal entity established for a specific asset, transaction, project, or investment strategy. In an asset tokenization structure, the SPV may:

- Own a property, receivable, loan, security, commodity, or other asset.

- Hold contractual rights against the asset owner.

- Issue equity, debt, fund units, or participation rights.

- Receive income generated by the asset.

- Distribute proceeds to eligible token holders.

- Separate the asset from liabilities elsewhere in the business group.

The token usually represents an interest issued by the SPV. Depending on the legal design, it may represent. This includes:

- Shares in the SPV.

- A debt claim against the entity.

- Units in a collective investment structure.

- Revenue or profit-participation rights.

- Contractual rights linked to an underlying asset.

- Beneficial ownership under an approved arrangement.

The token does not create enforceable ownership merely because it exists on a blockchain. Investor rights must be supported by company documents, subscription agreements, offering materials, asset-transfer records, registers, and applicable law. Blockchain records and automates the transaction. It does not replace securities, property, corporate, insolvency, taxation, or financial-services legislation.

Businesses choosing asset tokenization should therefore separate three components, and A robust SPV structure must align all three.

- The asset layer: Who legally owns the property, receivable, loan, security, or commodity?

- The investment layer: What enforceable rights does the investor receive?

- The technology layer: How are those rights issued, recorded, transferred, and administered on-chain?

Why Regulatory Flexibility Matters for SPV Tokenization?

For businesses, genuine flexibility means receiving clear answers to important commercial questions before capital is committed. The strongest jurisdictions provide a predictable route to compliance. Businesses should be cautious about descriptions such as A country can welcome virtual-asset companies while maintaining strict rules for crypto-friendly SPV structures or blockchain-friendly jurisdictions for securities, collective investment schemes, public fundraising, and financial promotions.

A suitable jurisdiction should clarify:

- Whether the token is a security, fund interest, debt instrument, virtual asset, or another regulated product.

- Whether a prospectus, private-placement exemption, notification, or approval applies.

- Which investors may participate.

- Whether the issuer, platform operator, adviser, custodian, broker, or marketplace requires authorization.

- How ownership and transfers are legally recorded.

- Whether smart-contract transfer restrictions are recognized operationally.

- How cross-border marketing is controlled.

- Which AML, KYC, sanctions, reporting, and recordkeeping obligations apply.

- Whether credible banks, administrators, auditors, custodians, and legal advisers support the model.

Top Regulation-Flexible Countries for SPV Tokenization

Jurisdiction | Strongest commercial use | Principal advantage | Important limitation |

Switzerland | Shares, bonds and institutional digital securities | Specific DLT securities and trading infrastructure | Securities and financial-services licences still apply |

UAE | MENA-focused securities, funds and selected property structures | Multiple specialized regulatory centres | ADGM, DIFC and VARA are separate regimes |

Singapore | Funds, private markets and institution-led products | Established securities regime and VCC structure | High governance and licensing expectations |

Luxembourg | EU funds, securitization and professional distribution | Mature institutional and EU financial ecosystem | Greater administration and substance requirements |

Liechtenstein | Specialized EEA token structures | TVTG framework for tokens and TT services | TVTG does not replace financial-market legislation |

Hong Kong | Funds, bonds and Asian institutional products | Detailed SFC tokenization guidance | Licensed intermediaries and approvals may be required |

United Kingdom | Tokenized funds and wholesale securities | Fund guidance and Digital Securities Sandbox | Sandbox access is not a general exemption |

Cayman Islands | Offshore funds and investment-holding SPVs | Flexible fund and corporate ecosystem | Investor-market laws still apply |

British Virgin Islands | Holding companies and private issuance vehicles | Flexible corporate structures and VASP framework | Less specific digital-securities infrastructure |

United States | Private placements, real estate and private credit | Deep capital markets and flexible state entities | Federal and state regulation is complex |

Malta | EU funds and developing tokenized-asset initiatives | EU membership and technology classification framework | Security tokens remain under financial-instrument rules |

Mauritius | Africa- and Asia-focused token structures | VAITOS framework and international financial centre | Securities, fund and cross-border rules require separate analysis |

Switzerland: Strong Legal Infrastructure for DLT Securities

Switzerland is one of the most developed jurisdictions for businesses requiring legal recognition of blockchain-recorded securities.

Swiss DLT legislation created a framework for DLT securities and introduced a licensing category for DLT trading facilities. FINMA licensed Switzerland’s first DLT trading facility in March 2025, showing that the framework is operational.

Swiss companies can be used as asset-holding or token-issuing vehicles. However, the structure may still trigger prospectus, financial-services, collective-investment, AML, custody, banking, or trading-venue requirements.

Best suited to:

- Tokenized company shares.

- Private debt and digital bonds.

- Institution-led tokenized securities.

- Private-market investment products.

- Structures requiring DLT-based ownership records.

- Businesses seeking a credible tokenized securities framework.

Business consideration: Switzerland provides strong legal infrastructure, but specialist legal, compliance, administration, and custody services can increase launch costs.

United Arab Emirates: Multiple Routes for MENA Tokenization

The UAE should not be treated as one unified tokenization jurisdiction. The most relevant regulatory environments include:

- Abu Dhabi Global Market and its Financial Services Regulatory Authority.

- Dubai International Financial Centre and its Dubai Financial Services Authority.

- Dubai mainland and non-DIFC free zones regulated for virtual assets by VARA.

- Federal and sector-specific requirements applying elsewhere in the UAE.

ADGM provides guidance covering digital-securities offers, listings, trading, settlement, and custody.

The DIFC operates under the DFSA. Its Investment Token framework covers security and derivative tokens. Updated Crypto Token rules took effect on January 12, 2026.

VARA regulates virtual-asset activities across Dubai’s mainland and free zones, excluding the DIFC. Its issuance framework includes different licensing, approval, white-paper, disclosure, and supervision requirements.

Best suited to:

- MENA-focused security-token platforms.

- Institutional private-market products.

- Tokenized bonds, sukuk, funds, or structured assets.

- Approved Real estate tokenization projects.

- Businesses able to maintain local governance and compliance operations.

Business consideration: The operating company, SPV, token issuer, property owner, and marketplace may fall under different UAE authorities.

Singapore: Strong for Institutional and Fund Tokenization

Singapore regulates shares, debentures, fund interests, and other capital-markets products through its established securities framework.

Offers may require a registered prospectus unless an exemption applies. Restricted schemes offered to accredited or other eligible investors may also require notification through Monetary Authority of Singapore systems.

Singapore’s Variable Capital Company structure is specifically designed for investment funds. A VCC can operate as a standalone vehicle or as an umbrella with multiple sub-funds.

However, a VCC is not automatically the best option for a single property or isolated asset. A company, trust, limited partnership, or alternative structure may be more suitable.

Best suited to:

- Tokenized investment funds.

- Private equity and private credit.

- Accredited-investor offerings.

- Institution-led assets tokenization platforms.

- Umbrella and multi-strategy fund products.

- Asian wealth and asset-management businesses.

Business consideration: Singapore is innovation-supportive but maintains strong expectations regarding licensed managers, governance, audit, administration, investor classification, and financial promotions.

Luxembourg: Strong for EU Funds and Institutional Distribution

Luxembourg is widely considered by businesses that need an established European fund, securitization, administration, and professional-services ecosystem.

The EU DLT Pilot Regime supports trading and settlement systems for crypto-assets that qualify as financial instruments under MiFID II.

Luxembourg’s CSSF supports the regime and has published guidance concerning the opportunities and risks associated with DLT in financial services.

Best suited to:

- Alternative investment funds.

- Tokenized fund units.

- Securitization vehicles.

- Professional-investor distribution.

- Institutional real-world asset portfolios.

- EU-oriented digital asset SPV formation.

Business consideration: Luxembourg is usually chosen for regulatory credibility, service providers, and distribution strategy rather than inexpensive company formation.

Liechtenstein: Specialized Token Structures Within the EEA

Liechtenstein is part of the European Economic Area but is not an EU member.

Its Token and TT Service Provider Act, known as the TVTG, establishes a framework for tokens and specified service providers using trusted technologies such as blockchain.

The TVTG does not replace financial-market legislation. A token representing a security, fund interest, banking product, or regulated investment may trigger separate licensing and compliance requirements.

Best suited to:

- Specialized token-right structures.

- EEA-focused digital-asset businesses.

- Smaller professional-investor offerings.

- Projects using locally regulated providers.

- Structures needing a formal token-service framework.

Business consideration: A TVTG registration should not be marketed as authorization to conduct securities dealing, investment management, custody, or public fundraising.

Hong Kong: Strong for Tokenized Funds and Bonds

Hong Kong has developed detailed guidance for tokenized securities and authorized investment products.

The Securities and Futures Commission requires intermediaries involved in tokenized securities to address staff expertise, due diligence, ownership records, technology risks, custody, and AML controls.

In April 2026, the SFC revised its framework for tokenized authorized investment products and published requirements for public secondary trading under defined conditions.

Best suited to:

- Tokenized investment funds.

- Tokenized bonds.

- Professional-investor products.

- Asian institutional distribution.

- Platforms working with licensed financial intermediaries.

Business consideration: Hong Kong supports tokenization within regulated finance. It does not provide unrestricted public distribution of SPV tokens.

United Kingdom: Strong for Funds and Wholesale Market Pilots

The United Kingdom provides two important routes: tokenized funds and controlled digital-securities infrastructure.

The FCA has published fund-tokenization guidance explaining how authorized managers can use distributed ledger technology within the existing regulatory framework.

The Digital Securities Sandbox, operated by the FCA and Bank of England, allows eligible businesses to test trading and settlement models under controlled conditions.

Best suited to:

- Tokenized investment funds.

- Wholesale securities.

- Regulated asset managers.

- Market-infrastructure pilots.

- Institutional financial-technology partnerships.

Business consideration: Financial-promotion, custody, dealing, collective-investment, market-infrastructure, and consumer-protection rules may apply separately.

Cayman Islands: Established Offshore Fund and SPV Ecosystem

The Cayman Islands is commonly used for investment funds, feeder structures, holding companies, and special-purpose issuers.

Its VASP framework requires relevant virtual-asset businesses to register or obtain the necessary licence. Licensing requirements for custody and virtual-asset trading platforms took effect in April 2025.

The legislation was amended in 2026 to address certain digital equity and investment tokens issued by tokenized funds.

This development makes Cayman particularly relevant for an Offshore SPV for tokenization involving funds or professional-investor structures.

Best suited to:

- Tokenized private funds.

- Tokenized mutual funds.

- Feeder and master-fund structures.

- Investment-holding SPVs.

- Cross-border private-market offerings.

Business consideration: A Cayman issuer does not remove securities, tax, marketing, or investor-protection requirements in the United States, European Union, United Kingdom, Asia, or other target markets.

British Virgin Islands: Flexible Corporate Vehicles for Private Structures

The British Virgin Islands provides flexible companies and limited partnerships commonly used for international holding and transaction structures.

The BVI Virtual Assets Service Providers Act took effect on February 1, 2023. It establishes registration and supervision requirements for businesses providing specified virtual-asset services from or within the BVI.

The BVI also maintains legislation for business companies, limited partnerships, beneficial ownership, economic substance, and segregated portfolio structures.

Best suited to:

- Private holding SPVs.

- Single-asset issuing companies.

- International joint ventures.

- Professional-investor token offerings.

- Cost-sensitive offshore corporate structures.

Business consideration: BVI company flexibility should not be confused with a specialized tokenized securities framework. Securities classification, fund regulation, VASP registration, investor-market rules, and banking availability must be analysed separately.

United States: Delaware and Wyoming Entity Flexibility With Federal Oversight

The United States offers deep capital markets, established private-placement routes, institutional investors, and a sophisticated legal-services ecosystem.

Delaware and Wyoming allow Series LLC structures that may support modular asset segregation when properly documented and operated.

However, a Series LLC does not create a securities exemption. Federal securities law, state securities law, tax, broker-dealer regulation, custody, transfer-agent requirements, beneficial-ownership reporting, and marketplace regulation may apply.

In January 2026, SEC divisions published a statement concerning the legal treatment of tokenized securities, reinforcing that tokenization changes the technical form of an instrument but not necessarily its legal classification.

Best suited to:

- Private placements.

- Tokenized real estate.

- Private credit and private equity.

- Delaware corporate or LLC structures.

- Businesses seeking access to US institutional capital.

- Platforms with experienced securities counsel.

Business consideration: Delaware and Wyoming offer entity flexibility, but neither state can independently authorize a nationwide tokenized-securities platform.

Malta: EU Financial Centre With Developing Tokenization Initiatives

Malta has a Virtual Financial Assets framework and an established financial-services regulator.

The MFSA uses a Financial Instrument Test to determine whether a DLT asset falls under existing EU financial legislation, the Virtual Financial Assets Act, or an exemption. A token qualifying as a financial instrument does not move into the VFA regime merely because it is issued using blockchain.

The MFSA has also published a position on tokenized fund units and launched a 2026 consultation concerning tokenized financial instruments and real-world assets.

Best suited to:

- Tokenized fund administration.

- EU-based pilot projects.

- Professional-investor structures.

- Businesses requiring EU legal alignment.

- Selected financial-instrument and RWA projects.

Business consideration: Malta should be evaluated as an EU financial jurisdiction, not as a light-touch destination for unrestricted security-token issuance.

Mauritius: Emerging Gateway for Africa and Asia

Mauritius operates an international financial centre and has enacted legislation specifically addressing virtual assets and initial token offerings.

The Virtual Asset and Initial Token Offering Services Act took effect in February 2022. It authorizes the Financial Services Commission to regulate VASPs and initial-token-offering issuers in the non-bank financial-services sector.

The framework includes capital, liquidity, custody, cybersecurity, risk-management, advertising, and reporting requirements for covered businesses.

Best suited to:

- Africa- and Asia-focused structures.

- International investment vehicles.

- Regulated virtual-asset operations.

- Professional-investor offerings.

- Projects requiring a lower-cost international financial centre.

Business consideration: The VAITOS framework does not automatically replace securities, collective-investment, company, tax, or target-market distribution requirements.

What Common Jurisdiction Claims Get Wrong?

“VARA provides absolute clarity for every token issuance”

VARA provides structured issuance categories, approvals, licensing requirements, disclosures, and supervision. The correct pathway depends on the token and the activities involved. Products issued from the DIFC fall under the DFSA rather than VARA.

“An EU company can distribute tokens throughout Europe”

EU market access is not automatic. Passporting depends on the regulated entity, licence, product, investor category, and applicable legislation.

MiFID II, AIFMD, the Prospectus Regulation, MiCA, national private-placement rules, and the DLT Pilot Regime may apply differently.

“Liechtenstein’s token model replaces securities law”

The TVTG creates a token and service-provider framework, but it remains separate from financial-market legislation.

“Cayman and BVI structures remove global securities obligations”

An offshore entity remains subject to the rules of every jurisdiction where tokens are promoted, sold, managed, custodied, or traded.

“Series LLCs automatically protect each asset”

Series structures can support asset segregation, but their effectiveness depends on documentation, separate accounting, operations, tax treatment, state law, and recognition in other jurisdictions.

What Are The Key Regulatory Factors to Evaluate Before Choosing a Jurisdiction?

Token classification

Classification determines which Asset tokenization regulations apply. Determine whether the token represents:

- Equity.

- Debt.

- A fund unit.

- A beneficial interest.

- Revenue participation.

- A derivative.

- Direct asset ownership.

- A virtual asset outside securities law.

Investor location

A company must analyse where investors reside, where marketing occurs, which websites or applications are accessible, and whether private-placement or professional-investor restrictions apply. Identify whether the business will:

- Issue tokens.

- Arrange investments.

- Advise investors.

- Manage assets.

- Hold client funds.

- Control private keys.

- Operate an order book.

- Match buyers and sellers.

- Settle trades.

- Process redemptions.

- Convert fiat and digital assets.

Each function may create a separate regulatory obligation.

Asset location

All assets remain governed by the laws controlling their ownership and transfer. An offshore issuer cannot override local land-registration or foreign-ownership restrictions.

Banking and custody

Before completing digital asset SPV formation, confirm whether banks, payment providers, administrators, and custodians will support:

- The jurisdiction.

- The intended asset.

- Target investors.

- Fiat subscriptions.

- Stablecoin settlement.

- Token custody.

- Cross-border payments.

- Income distributions.

Tax and economic substance

A low headline rate does not guarantee a tax-efficient structure. Always review:

- Corporate taxation.

- Withholding.

- Transfer duties.

- Property taxes.

- Investor reporting.

- Treaty access.

- Economic substance.

- Management and control.

- Permanent establishment.

- Exit taxation.

10 Step Process : SPV Tokenization Regulatory Framework

Step 1: Define the Commercial Product

Clearly define the underlying asset, funding target, investor profile, revenue model, holding period, redemption rights, governance structure, and intended transfer market. A well-designed commercial model is the foundation of successful asset tokenization, helping determine the most suitable crypto-friendly SPV structures, investor protections, and regulatory pathway.

Step 2: Classify the Token

Obtain a detailed legal opinion on whether the token qualifies as a security, financial instrument, fund interest, or virtual asset. The analysis should address offering requirements, exemptions, investor restrictions, and marketing limitations. Accurate classification ensures compliance with the applicable tokenized securities framework and relevant asset tokenization regulations.

Step 3: Design the Jurisdiction Stack

Cross-border tokenization may involve four separate legal locations: the asset jurisdiction, SPV or issuer jurisdiction, platform-operator jurisdiction, and investor-distribution jurisdictions. Businesses should compare tokenization-friendly jurisdictions and blockchain-friendly jurisdictions to create an efficient structure that supports compliance, taxation, investor access, enforceability, and long-term scalability.

Step 4: Select the Appropriate Vehicle

Choose a legal vehicle that matches the asset, investor base, governance model, and fundraising strategy. Options may include a company, LLC, Series LLC, limited partnership, fund, VCC, trust, foundation, or securitization vehicle. An offshore SPV for tokenization may provide greater flexibility for international offerings and asset segregation.

Step 5: Establish Strong Governance

Define director duties, conflicts-of-interest procedures, reserved matters, voting thresholds, valuation policies, borrowing limits, distributions, asset disposals, defaults, and winding-up procedures. Effective governance strengthens investor confidence and protects the underlying asset. It is particularly important when establishing digital asset SPV formation across multiple regulatory and operational jurisdictions.

Step 6: Transfer or Secure the Asset

The SPV must obtain legally enforceable ownership, security, or control over the underlying asset. This may involve title transfer, assignment, custody, escrow, collateral arrangements, or security registration. Effective asset control ensures that token-holder rights are supported by recognized legal mechanisms, rather than relying solely on blockchain technology.

Step 7: Prepare the Offering Documents

Offering documents must clearly explain what each token represents, investor rights, fees, valuation methods, distributions, redemption terms, governance, custody, transfer restrictions, technology risks, defaults, and dispute resolution. Transparent documentation is essential under most asset tokenization regulations and helps investors understand both the commercial opportunity and associated legal risks.

Step 8: Identify Regulated Activities

Map every service involved in the tokenization process, including placement, brokerage, investment management, fund administration, transfer agency, custody, payments, and marketplace operation. Determine which functions may be performed internally and which require licensed providers. This assessment is central to building a compliant tokenized securities framework across multiple jurisdictions.

Step 9: Convert Legal Rules into Platform Controls

Translate regulatory obligations into automated platform controls, including KYC, KYB, investor classification, sanctions screening, wallet monitoring, country restrictions, whitelisting, lock-up periods, ownership limits, voting, corporate actions, distributions, audit trails, and reporting. Combining legal rules with blockchain technology creates a more secure, transparent, and enforceable tokenization system.

Step 10: Audit and Launch

Before launch, review the smart contracts, legal documents, custody arrangements, investor journey, payment flows, disclosures, and operational procedures as one connected system. The selected structure should be tested against the requirements of Flexible Countries for SPV tokenization, ensuring that legal rights, technology, compliance, and asset ownership remain fully aligned.

Real Estate Tokenization vs. Fund Tokenization

Real Estate Tokenization

In real estate tokenization jurisdictions, the property’s location is usually the primary legal anchor. The structure must address land registration, foreign ownership, transfer taxes, mortgage consent, leases, property management, valuation, insolvency, and title enforcement. Token holders generally own shares or debt issued by the property SPV, not direct building ownership.

Fund Tokenization

Fund tokenization focuses on the fund domicile, manager authorization, administration, custody or depositary requirements, net asset value, subscriptions, redemptions, portfolio restrictions, investor classification, and distribution permissions. Singapore VCCs, Luxembourg vehicles, Cayman funds, Malta funds, and UK structures offer different benefits within global tokenization-friendly jurisdictions and regulated investment markets.

Requirement | Real estate SPV | Tokenized fund |

Primary legal anchor | Property location | Fund and manager domicile |

Typical investor right | SPV shares, debt or revenue claim | Fund shares or units |

Key operational data | Title, rent, expenses and property value | NAV, subscriptions and portfolio value |

Main regulatory focus | Property, securities and promotion | Funds, management and distribution |

Common structure | One SPV per property or portfolio | Standalone fund or umbrella |

Major investor concern | Enforceability against the asset | Governance, valuation and liquidity |

Common Mistakes To Avoid When Selecting Tokenization-Friendly Jurisdictions

- Choosing based only on incorporation cost- A low-cost company can become unusable when banking, custody, administration, insurance, or regulated partners are unavailable.

- Confusing company formation with offering authorization- Registering an SPV does not authorize it to conduct a securities offering.

- Confusing VASP registration with securities licensing- Virtual-asset permissions may not cover investment management, brokerage, financial advice, security-token trading, or fund administration.

- Ignoring investor jurisdictions- An offshore SPV cannot legally market everywhere merely because the issuer is incorporated.

- Building the token before defining legal rights- Smart-contract logic should follow the ownership, income, governance, transfer, redemption, and default rules.

- Assuming tokenization creates liquidity- Blockchain can improve transfer administration. It cannot guarantee buyers, exchange admission, pricing, or lawful secondary trading.

- Misrepresenting property ownership- Businesses should not claim that investors own direct property title when they only own securities or contractual rights issued by an SPV.

- Ignoring insolvency and creditor priority- Token holders may rank behind secured lenders, tax authorities, employees, administrators, and other creditors.

- Selecting one jurisdiction for every business function- The asset owner, issuer, manager, technology operator, custodian, and investors may require separate legal locations.

How to Choose the Right SPV Jurisdiction for Your Business?

For choosing the right SPV jurisdiction for your business, use a weighted scorecard rather than a generic ranking.

Decision factor | Recommended priority |

Token-classification certainty | Very high |

Target-investor access | Very high |

Asset-ownership compatibility | Very high |

Required licences and exemptions | Very high |

Banking and custody availability | Very high |

Regulated service-provider access | High |

Tax and economic substance | High |

Secondary-transfer pathway | High |

Setup and annual costs | High |

Regulatory engagement | Medium |

Incorporation speed | Medium |

Founder convenience | Low |

Reject a jurisdiction when it fails a critical commercial requirement, even when its overall score appears attractive.

- Choose Switzerland when: You need recognized DLT securities infrastructure and institutional credibility.

- Choose ADGM or DIFC when: You are targeting MENA investors and require regulated financial-services infrastructure.

- Choose Singapore when: You are building an institution-led fund or private-market platform for Asian investors.

- Choose Luxembourg when: You require an EU fund, securitization, or professional-investor structure.

- Choose Liechtenstein when: You need a specialized token-services framework within the EEA.

- Choose Hong Kong when: You are targeting Asian funds, bonds, and institutional capital through licensed intermediaries.

- Choose the United Kingdom when: Your model involves tokenized funds or controlled wholesale market-infrastructure testing.

- Choose Cayman when: You require an offshore private-fund, feeder, or investment-holding structure.

- Choose BVI when: You need a flexible private holding or issuing SPV and can manage cross-border compliance separately.

- Choose Delaware or Wyoming when: Your product targets the United States, and you have experienced federal and state securities counsel.

- Choose Malta when: You need an EU jurisdiction for funds or an emerging tokenized-financial-instrument project.

- Choose Mauritius when: Your commercial strategy focuses on Africa, Asia, or an international financial-centre structure.

How Does SPV Tokenization Work Globally?

The following are the step-by-step instructions showing how SPV tokenization works globally:

- Establish the SPV in a jurisdiction based on the asset, investors, tax, and licensing requirements.

- Transfer or secure the underlying asset through title, assignment, custody, escrow, or collateral.

- Define token-holder rights covering ownership, income, voting, redemption, and transfers.

- Obtain regulatory approvals or rely on documented exemptions.

- Verify investors through KYC, KYB, sanctions, accreditation, and source-of-funds checks.

- Issue tokens after legal documents, smart contracts, custody, and payment systems align.

- Synchronize blockchain records with ownership registers.

- Distribute income through approved payment channels.

- Allow transfers only after compliance checks.

- Redeem tokens, sell assets, refinance, or wind down the SPV according to offering documents.

TakeAway

Choosing among Flexible Countries for SPV tokenization requires more than comparing tax rates or incorporation speed. The strongest tokenization-friendly jurisdictions combine enforceable ownership, investor protection, banking, custody, lawful issuance, and controlled secondary transfers. Whether pursuing Real estate tokenization, crypto-friendly SPV structures, an offshore SPV for tokenization, or digital asset SPV formation, businesses must align asset tokenization regulations, Blockchain technology, service providers, and target investors within one workable tokenized securities framework.

Ready to Launch? Partner With Shamla Tech Before Compliance Delays Cost You

At Shamla Tech, we turn approved SPV tokenization requirements into secure, scalable, investor-ready platforms. Our Tokenization Development Company builds token issuance systems, smart contracts, KYC/AML workflows, investor dashboards, custody integrations, automated distributions, wallet controls, reporting, and controlled marketplaces around your chosen SPV structure and operating model. By integrating compliance requirements from day one, we help reduce costly redevelopment, accelerate market readiness, and strengthen investor confidence. Partner with us to launch an enterprise-grade real-world asset or real estate tokenization platform built for growth.

FAQs

1. Which countries are most flexible for SPV tokenization?

Switzerland, the UAE, Singapore, Luxembourg, Liechtenstein, Hong Kong, the UK, Cayman Islands, BVI, United States, Malta, and Mauritius can each support specific tokenization models. The best choice depends on the asset, investors, platform activities, and intended distribution markets.

2. Are SPV tokens always securities?

Not automatically. However, tokens representing shares, debt, fund interests, profits, income, or investment returns frequently fall within securities or financial-instrument legislation.

3.Can a Cayman or BVI SPV sell tokens globally?

No. The offering must comply with the rules of every jurisdiction where investors are targeted or admitted.

4.Which jurisdiction is best for real estate tokenization?

The property’s location usually determines the core ownership and title requirements. The issuer may be established elsewhere, but local property and securities rules remain relevant.

5.Which jurisdiction is best for fund tokenization?

Singapore, Luxembourg, Cayman, Malta, the United Kingdom, Hong Kong, and other established fund centres may be suitable depending on the manager, investors, strategy, and distribution markets.

6.What should a SPV tokenization platform include?

Core features normally include investor onboarding, KYC/KYB, wallet screening, investor classification, transfer controls, cap-table management, document storage, distributions, voting, custody integrations, reporting, and audit trails.

7.Should a company choose the jurisdiction before building the platform?

Yes. Token classification, investor rules, transfer restrictions, licensing, governance, custody, and reporting requirements directly affect the platform architecture.