FCA-compliant RWA Tokenization Platform development in the UK tokenization market is gaining traction for businesses. Banks, asset managers, fintech firms, and investment platforms are exploring tokenized real estate, private credit, funds, bonds, and commodities to improve liquidity, reduce manual operations, and open fractional investment access.

To build trust, firms must align innovation with FCA tokenization UK expectations. A compliant platform needs AML checks, investor verification, custody controls, financial promotion compliance, smart contract security, transparent reporting, and strong governance under evolving UK blockchain regulations. In 2026, the UK is moving from policy discussion to regulatory execution. The FCA says crypto firms will be able to start applying for authorisation from 30 September 2026, while the wider UK cryptoasset regime is expected to come into force in October 2027. Until then, crypto remains largely regulated for financial promotions and financial crime purposes, while tokenized securities, funds, and market infrastructure can already fall under existing rules. This guide explores how to launch an FCA-compliant Tokenization Platform in the UK in 2026.

What “FCA-Compliant” Means for UK RWA Tokenization in 2026?

For UK firms, FCA tokenization UK does not mean one simple licence covers every use case. It means the platform must be mapped against the correct regulatory perimeter.

A tokenized bond is not treated the same as a tokenized warehouse receipt. A tokenized fund unit is not the same as a tokenized loyalty asset. A marketplace for security tokens is not the same as a private issuance portal for professional investors. In 2026, businesses must think in layers:

Compliance layer | What it covers | Why it matters |

Asset classification | Whether the token represents securities, fund units, stablecoins, commodities, debt, property, or other rights | Defines the regulatory route |

Financial promotions | How the offer is marketed to UK users | Prevents unlawful promotion |

AML/CTF/PF controls | KYC, sanctions, transaction monitoring, suspicious activity reporting | Protects the platform from financial crime |

Custody and safeguarding | Who controls assets, wallets, keys, and investor records | Protects client assets |

Trading and settlement | Whether the platform enables secondary trading, matching, or transfer | May trigger trading venue or cryptoasset activity rules |

Governance and conduct | Board oversight, risk controls, complaints, disclosures, conflicts | Supports FCA expectations |

Technology controls | Smart contract audits, cybersecurity, resilience, monitoring | Reduces operational risk |

The UK government passed legislation in February 2026 to create a financial services regulatory framework for cryptoassets, and HM Treasury has continued refining how stablecoins and tokenised payments fit into the regime.

So the smart move is not to wait until 2027. UK firms should build platforms in 2026 that are authorisation-ready, audit-ready, and regulator-ready.

Why UK Firms Are Building Regulated RWA UK Platforms Now?

The business case for regulated RWA UK platforms is about capital efficiency. Traditional private markets are slow. Asset onboarding is manual. Investor subscriptions take time. Transfers require paperwork. Ownership records sit across spreadsheets, fund administrators, custodians, and legal documents.

A well-built tokenization platform improves this by creating a programmable ownership layer. For businesses, this can unlock:

- Faster asset issuance

- Fractional investor access

- New revenue from issuance, custody, trading, servicing, and administration

- Lower reconciliation cost

- Better investor reporting

- Faster settlement workflows

- Reusable compliance infrastructure

- Wider distribution across eligible investors

The FCA and Bank of England have said tokenisation could streamline wholesale markets, making securities issuance, asset management, and settlement faster and more efficient. They also said the industry wants clearer regulation and infrastructure as tokenisation grows.

That is the ROI angle business leaders care about. Tokenization is valuable when it lowers friction in capital formation and asset lifecycle management.

What Are The Regulatory Requirements for an FCA Compliant RWA Tokenization Platform UK 2026

A reliable platform must answer compliance questions before writing code.

- Asset Classification

The first step is deciding what the token represents. It may represent equity, debt, fund units, real estate rights, invoices, commodities, carbon credits, revenue rights, or another asset-linked claim.

This classification decides whether the platform falls under securities law, collective investment scheme rules, cryptoasset rules, property law, commodities regulation, or a combination of these.

- FCA Authorisation and Permissions

Businesses must check whether they need FCA authorisation for activities such as dealing, arranging, safeguarding, operating a trading platform, issuing qualifying stablecoins, or supporting staking.

The FCA’s future crypto regime guidance identifies regulated cryptoasset activities such as issuing qualifying stablecoin, operating trading platforms, dealing and arranging deals, safeguarding cryptoassets, and staking.

A UK RWA platform should not assume it can operate first and “become compliant later.” That approach creates licensing, marketing, banking, custody, and enforcement risk.

- Financial Promotions

Financial promotions matter from day one. If the platform markets tokenized assets to UK consumers, promotions must be fair, clear, and not misleading.

The FCA’s cryptoasset financial promotion rules include clear risk warnings, banning incentives to invest, positive frictions, client categorisation, and appropriateness assessments. The regime applies to firms marketing cryptoassets to UK consumers, including overseas firms.

For a tokenized asset platform in the UK, this means landing pages, ads, emails, app screens, investor decks, webinars, referral offers, and onboarding flows may all need compliance review.

- AML, CTF, and Proliferation Financing Controls

A platform must verify investors and monitor transactions. This includes KYC, KYB, sanctions screening, politically exposed person checks, wallet screening, transaction monitoring, source-of-funds checks, and suspicious activity reporting.

Weak AML controls can block banking partnerships, delay authorisation, and damage investor trust.

- Consumer Duty and Investor Outcomes

The FCA’s minimum standards page highlights threshold conditions, fit and proper expectations, high-level standards, Principles for Businesses, and the Consumer Duty. Firms must show appropriate resources, suitable business models, effective supervision, and good outcomes for retail customers where relevant.

For regulated RWA UK products, this means the platform must explain risks clearly, avoid misleading yield claims, show fees, manage conflicts, and provide support when things go wrong.

- Custody and Safeguarding

Custody is one of the hardest parts of RWA tokenization. The platform must define who controls the underlying asset, who controls the tokens, who controls private keys, and who reconciles on-chain balances with off-chain legal records.

This is especially important when the asset is a fund unit, security, gold reserve, property interest, or debt instrument.

- Data Protection and Cyber Security

A UK platform will process identity data, financial data, wallet data, bank information, and investment records. GDPR, cyber security, data retention, access control, and incident response must be built into the system.

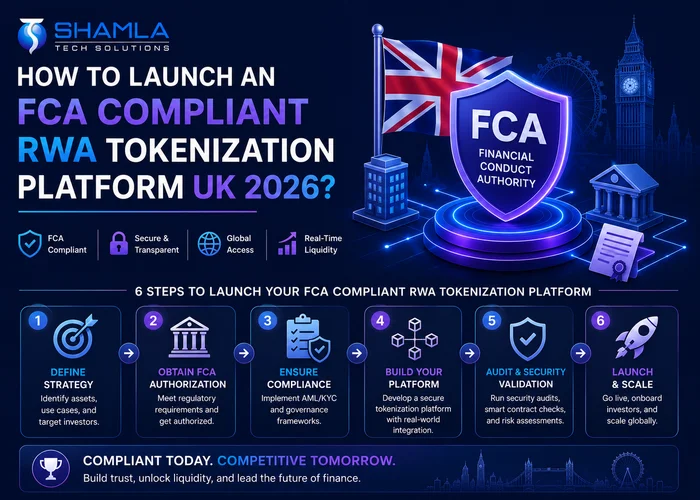

Step-by-Step: How to Build an FCA-Compliant RWA Tokenization Platform in the UK

- Define the Asset and Commercial Model

Choose the RWA category first. A platform for tokenized bonds needs different workflows than a real estate, private credit, carbon credit, invoice finance, or gold-backed token platform.

- Map the Regulatory Perimeter

Identify whether the product falls under existing securities rules, fund rules, financial promotions, AML obligations, DSS scope, future cryptoasset permissions, or payment regulations.

- Create the Legal Structure

Use the right structure, such as an SPV, fund, trust, nominee model, contractual claim, direct ownership model, or register-linked structure. The token must connect to enforceable rights.

- Design the Investor Eligibility Framework

Define whether the product targets retail investors, professional investors, high-net-worth investors, sophisticated investors, institutions, or a closed private network.

- Build the Compliance Workflow

Add KYC, KYB, AML, sanctions screening, risk scoring, wallet screening, suitability checks, jurisdiction controls, investor categorisation, and audit records.

- Develop Smart Contracts

Smart contracts should handle issuance, burning, transfer restrictions, lockups, investor whitelisting, income distribution, redemption, cap table updates, and compliance rules.

- Add Custody and Asset Verification

Connect the platform with regulated custodians, trustees, asset managers, registrars, vaults, or administrators, depending on the asset class.

- Build the Investor Platform

Develop investor dashboards, asset pages, disclosure screens, subscription flows, wallet integration, payment rails, reporting, document access, and support features.

- Add Admin and Compliance Control Panels

The platform team needs tools to approve investors, pause transfers, freeze wallets, update asset records, manage payouts, monitor risks, and produce audit reports.

- Test, Audit, and Launch

Run smart contract audits, penetration tests, compliance simulations, investor journey reviews, financial promotion checks, disaster recovery tests, and legal sign-offs before launch.

Architecture Requirements for a Tokenized Asset Platform UK

An FCA-ready platform needs more than a token engine. It needs a modular architecture that allows the business to prove control.

Architecture layer | Required capability | Business value |

Asset onboarding layer | Asset verification, valuation, documents, and ownership records | Reduces bad-asset risk |

Legal rights layer | SPV, trust, fund, nominee, or contractual framework | Connects tokens with enforceable rights |

Compliance layer | KYC, AML, sanctions, investor categorisation, jurisdiction rules | Supports FCA readiness |

Smart contract layer | Issuance, transfer rules, cap table, distributions, redemption | Automates asset lifecycle |

Custody layer | Asset custody, token custody, key management, wallet policies | Protects assets and users |

Payment layer | Fiat rails, stablecoin support where permitted, reconciliation | Supports subscriptions and payouts |

Investor portal | Dashboards, disclosures, reports, portfolio view | Improves investor trust |

Admin console | Compliance review, asset management, reporting, support | Improves operational control |

Marketplace layer | Controlled secondary transfers or trading workflows | Supports liquidity |

Audit and monitoring layer | Logs, alerts, reports, SIEM, blockchain analytics | Supports supervision and resilience |

This is where UK blockchain regulations influence architecture. The system must show not only that a token exists, but also that every token transfer follows the correct business, legal, and compliance rules.

How FCA-Compliant Tokenization Helps UK Businesses Generate Revenue

A business should not build an FCA-compliant RWA Tokenization Platform UK 2026 just because competitors are discussing tokenization. It should build one when the economics are clear.

Revenue stream | How the business earns |

Issuance fees | Charge asset owners to tokenize assets |

Investor subscription fees | Charge for access, onboarding, or transaction processing |

Servicing fees | Manage reporting, distributions, investor relations, and asset records |

Custody or wallet fees | Charge for secure asset or token custody services where permitted |

Marketplace fees | Earn from controlled secondary transfers or trading activity |

White-label licensing | Offer the platform to funds, issuers, brokers, or asset managers |

Data and analytics | Provide valuation, liquidity, investor, and risk analytics |

Revenue Models Cost Savings

Tokenization can also reduce operating costs by automating manual tasks. Subscription processing, investor onboarding, ownership updates, transfer approvals, distribution calculations, and reconciliation can become faster and more auditable.

Capital Formation

The biggest ROI may come from wider investor access. Fractional ownership can help asset owners reach more eligible investors without selling an entire asset. This can work especially well for real estate, private credit, funds, commodities, infrastructure, and income-generating assets.

How Investors Benefit From Regulated RWA UK Platforms?

Investors do not care that a platform uses blockchain. They care about access, clarity, safety, liquidity, and returns. A strong, regulated RWA UK platform gives investors:

- Lower minimum investment sizes

- Clear asset details and disclosures

- Transparent ownership records

- Digital portfolio tracking

- Faster subscription and redemption workflows

- Potential access to secondary liquidity

- Automated income distributions

- Better audit trails

- Stronger identity and fraud controls

The FCA’s strengthened promotion expectations focus on clear information, time for consumers to reflect, appropriateness, record keeping, and due diligence. That shows why investor journeys must be designed carefully, not only beautifully.

What UK Firms Should Consider Before Building FCA Complaint Real World Asset Tokenization Platform.

Before starting FCA Complaint Real World Asset Tokenization Platform development, business leaders should answer these questions:

- What asset class will be tokenized first?

Start with one asset type. A platform that tries to tokenize everything usually builds weak workflows for everything.

- Who is the target investor?

Retail, professional, institutional, and overseas investors create different compliance obligations.

- Will the platform support secondary transfers?

Secondary liquidity sounds attractive, but it may trigger more complex trading, matching, custody, and market conduct rules.

- Who will have custody of the asset and tokens?

The business needs a clear separation between asset custody, wallet custody, issuer control, and investor access.

- How will financial promotions be approved?

Marketing must be built into compliance review, not handled by growth teams alone.

- Will the platform use public, private, or permissioned blockchain infrastructure?

Public chains offer transparency and ecosystem access. Permissioned models offer more control. Hybrid models often work best for regulated markets.

- How will the business prove ROI?

Define platform KPIs before launch: assets onboarded, investor conversion, cost per investor, settlement time, issuance cost, liquidity, and servicing margin.

Best Blockchain and Token Standards for FCA Tokenization UK

There is no single best blockchain for FCA tokenization in the UK. The right choice depends on investor type, asset type, privacy needs, compliance controls, cost, liquidity, and institutional acceptance.

Option | Best use case |

Ethereum | Institutional familiarity, security token standards, ecosystem depth |

Polygon | Lower fees, EVM compatibility, faster retail-friendly experience |

Avalanche | Subnet flexibility and enterprise asset networks |

Polymesh | Regulated asset and compliance-native workflows |

Hyperledger Besu | Permissioned enterprise networks |

Private DLT | Closed institutional networks and sensitive financial data |

Hybrid architecture | Public proof with private compliance and asset data |

Useful token standards include ERC-1400, ERC-3643, ERC-20 with transfer restrictions, and custom security token standards. The main rule is simple: the token standard must support compliance enforcement.

Digital Securities Sandbox and Wholesale Market Opportunities

The Digital Securities Sandbox is a major opportunity for firms that want to test tokenized securities infrastructure under regulatory supervision.

The Bank of England explains that the DSS is a regulated live environment for using technologies such as distributed ledgers in the issuance, trading, and settlement of securities in the UK. It supports activities such as notary, maintenance, settlement, and trading venue operation for financial securities.

The FCA says activity after Gate 2 involves issuing, trading, and settling real digital securities. Examples include equities, corporate and government bonds, money market instruments, fund units, and emissions allowances. The DSS is open to UK-established firms of all sizes, including existing authorised institutions and new entrants.

For businesses building regulated RWA UK infrastructure, the DSS matters because it offers a controlled route to test live market infrastructure without waiting for every permanent market rule to mature.

Risk Controls Every FCA-Ready RWA Platform Needs

An RWA platform must control legal, financial, operational, and technical risk.

Risk | How to control it |

Asset misrepresentation | Asset verification, valuation, legal documents, proof-of-asset records |

Investor ineligibility | KYC, investor categorisation, jurisdiction rules, access controls |

Unlawful promotion | Approval workflows, risk warnings, compliance review, and record keeping |

Smart contract failure | Independent audits, formal verification, bug bounty, pause functions |

Cyber attack | MFA, encryption, wallet policies, penetration testing, monitoring |

Custody failure | Regulated custodians, segregation, reconciliation, and key management |

Low liquidity | Market maker strategy, redemption model, controlled secondary market |

Regulatory change | Modular compliance engine, policy updates, legal monitoring |

Operational failure | Incident response, business continuity, disaster recovery |

Conflicts of interest | Clear disclosures, governance, and independent review |

This is why compliance should be embedded into the platform architecture. If compliance depends on manual checks after launch, the platform will not scale safely.

Estimated Cost and Timeline

The cost to build an FCA-compliant RWA Tokenization Platform UK 2026 depends on product complexity.

Platform type | Typical scope | Timeline expectation |

MVP issuance portal | Asset pages, KYC, token issuance, investor dashboard | Faster build, limited market features |

Compliance-ready private issuance platform | KYC/KYB, transfer restrictions, smart contracts, admin controls, reporting | Medium complexity |

Full RWA marketplace | Issuance, custody, secondary transfers, payment rails, compliance engine, analytics | High complexity |

Institutional DSS-style infrastructure | Notary, settlement, trading, custody, regulatory reporting | Highest complexity |

The cheapest build is rarely the best build. UK firms should budget for legal advice, compliance design, smart contract audits, penetration testing, custody integration, payment integration, ongoing monitoring, and regulatory change management.

Common Mistakes UK Firms Must Avoid

- Building the Token Before the Legal Model

A token without enforceable rights is a weak product. Start with the legal structure, then build the token.

- Ignoring Financial Promotions

Marketing can trigger regulatory risk before the first investor buys. Review all public and private communications.

- Treating KYC as a Plugin

KYC must connect with transfer rules, wallet access, jurisdiction restrictions, and investor eligibility.

- Promising Liquidity Too Early

Secondary markets require careful regulatory analysis. Do not promise easy exits unless the liquidity route is real.

- Using One Smart Contract for Every Asset

Different assets need different rights, transfer rules, lockups, payout logic, and reporting.

- Forgetting Off-Chain Reconciliation

The blockchain record must match the legal register, custodian records, payment data, and asset documentation.

- Choosing Blockchain Before Business Model

A chain decision should follow asset type, investor base, privacy needs, and regulatory constraints.

Future of UK Blockchain Regulations for RWA Platforms

The FCA and Bank of England have opened a call for input on the future of tokenisation in UK wholesale markets, saying tokenisation could be one of the most consequential changes to wholesale markets for decades. They also aim to publish a joint response and roadmap later in 2026.

The FCA has also published guidance to support fund tokenisation within existing rules, including how firms can use DLT and an optional Direct to Fund model to make fund dealing more efficient.

For UK firms, this creates a clear message: the opportunity is real, but the winning platforms will be built with compliance, governance, and market infrastructure in mind.

TakeAway

Building an FCA-compliant RWA Tokenization Platform UK 2026 is not a normal software project. It is a regulated financial infrastructure project with blockchain at its core.

The platform must prove asset backing, investor eligibility, compliant promotion, custody control, smart contract security, payment integrity, auditability, and operational resilience. It must also generate ROI through faster issuance, better investor access, lower administration, and new revenue channels.

The firms that win in regulated RWA UK will not be the ones that launch the fastest demo. They will be the ones that build trusted infrastructure early, prepare for authorisation, and give investors a safer way to access real-world assets digitally.

For UK businesses, 2026 is the preparation year. The best time to build the compliance architecture is before the market becomes crowded.

Launch Your FCA-Compliant Tokenization Platform With ShamlaTech

If you want to launch an FCA-compliant RWA Tokenization Platform UK 2026, ShamlaTech helps you move from regulatory planning to production-ready execution. You can build a platform that supports asset onboarding, issuer controls, KYC/AML, custody integrations, automated reporting, and marketplace modules for primary issuance and secondary trading. ShamlaTech’s RWA tokenization platform development services also support assets like real estate, commodities, and fine art as secure, tradable digital tokens. With the right architecture, you can unlock liquidity, enable fractional ownership, improve transparency, and serve investors with stronger confidence