Financial institutions are entering a new phase of asset ownership, distribution, and liquidity management through RWA tokenization. Banks, funds, and asset issuers are integrating blockchain infrastructure to improve capital access, automate operations, and expand participation across private and institutional markets.

Global banks are projected to move more than $5 trillion in tokenized digital securities and fund assets by 2030, as financial institutions expand investments into tokenized bonds, private credit, treasury products, and alternative asset infrastructure. This institutional demand is accelerating the need for enterprise-grade RWA tokenization platforms designed for compliance, scalability, and regulated asset management.

This article explores 10 major RWA tokenization use cases for banks, funds, and asset issuers in 2026. It also explains how institutions generate revenue through tokenized assets and outlines the key steps required to build an RWA tokenization platform for financial services.

Why Are Banks, Funds, and Asset Issuers Exploring RWA Tokenization in 2026?

Banks, funds, and asset issuers are integrating RWA tokenization to improve asset liquidity, reduce settlement dependencies, expand investor access, and create programmable financial products. Institutional adoption is being driven by measurable operational and capital market advantages across debt, funds, private credit, and real estate issuance.

Why Institutions Are Investing in RWA Tokenization Platforms

- Tokenized assets enable financial institutions to distribute traditionally illiquid assets across a broader investor base through fractional ownership structures and digital issuance models.

- Banks are using tokenization infrastructure to reduce settlement timelines, automate compliance workflows, and improve collateral mobility across cross-border financial operations.

- An industry survey found that 65% of asset managers with tokenized funds reported operational and distribution advantages over traditional fund structures, reinforcing institutional demand for dedicated RWA tokenization platforms.

- Asset issuers are launching tokenized bonds, treasury products, and private credit offerings to improve fundraising efficiency and enable programmable distribution mechanisms.

- Institutional-grade RWA tokenization platforms provide integrated capabilities for investor onboarding, compliance management, digital custody, secondary trading, and multi-asset issuance within a unified infrastructure layer.

10 RWA Tokenization Use Cases for Banks, Funds, and Asset Issuers in 2026

1. Real Estate Tokenization

2. Private Equity Fund Tokenization

3. Private Credit and Debt Instrument Tokenization

4. Government Bonds and Treasury Asset Digitization

5. Money Market Fund Tokenization

6. Trade Finance Asset Distribution

7. Commodity and Precious Metal Tokenization

8. Carbon Credit and ESG Asset Markets

9. Mining Reserve Tokenization

10. Invoice Financing and Receivables Tokenization

Revenue Opportunities Behind These RWA Tokenization Use Cases for Banks, Funds, and Asset Issuers

Use Case | Banks | Funds | Asset Issuers |

Real Estate Tokenization | Collateralized lending revenue | Fractional property exposure | Faster capital formation |

Private Credit Tokenization | Syndicated debt servicing | Yield-focused credit products | Automated debt issuance |

Treasury Asset Digitization | Faster collateral mobility | Institutional fixed-income access | Digital sovereign distribution |

Money Market Fund Tokenization | Treasury infrastructure fees | Real-time liquidity allocation | 24/7 fund accessibility |

Trade Finance Tokenization | Cross-border settlement revenue | Trade receivable participation | Faster invoice financing |

Commodity Tokenization | Commodity-backed lending | Precious metal exposure | Reserve monetization |

Carbon Credit Markets | ESG infrastructure revenue | Sustainable asset products | Carbon asset trading |

Mining Reserve Tokenization | Resource financing products | Reserve-backed investment access | Alternative fundraising |

Invoice Receivable Tokenization | Financing spreads | Short-duration yield access | Working capital acceleration |

The Market Potential Behind Institutional RWA Tokenization:

- The tokenized asset market is projected to reach $16 trillion by 2030, driven by institutional demand across private credit, real estate, treasury products, and alternative investments.

- The global trade finance gap exceeded $2.5 trillion, creating large-scale opportunities for banks and funds to monetize tokenized receivables, invoices, and cross-border financing infrastructure.

- Carbon credit markets are expected to surpass $100 billion by 2030, creating new institutional revenue opportunities across ESG trading, sustainability finance, and environmental asset distribution.

- The private credit market surpassed $1.7 trillion in assets under management, accelerating demand for tokenized debt issuance, servicing infrastructure, and institutional liquidity solutions.

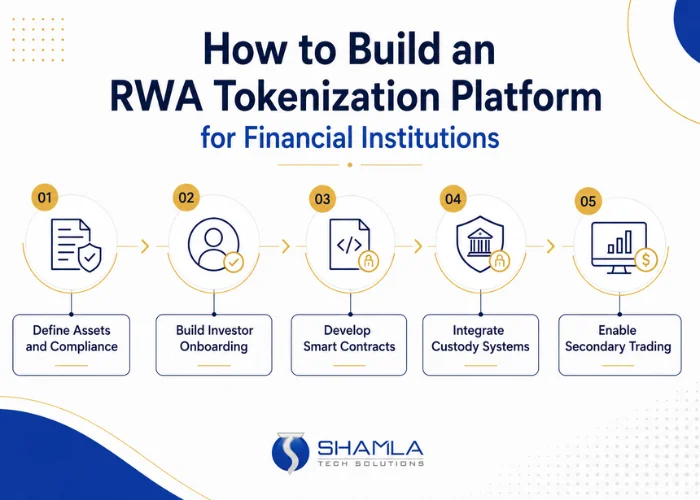

How to Build an RWA Tokenization Platform for Financial Institutions

Key Steps to Build an Institutional RWA Tokenization Platform:

- Define Asset Structures and Regulatory Requirements

Institutional RWA platforms must be designed around specific asset classes, investor categories, and jurisdictional regulations before development begins. Banks and asset issuers need frameworks that align with securities compliance, investor restrictions, custody obligations, and cross-border distribution requirements across markets such as the United States, Singapore, and United Arab Emirates.

- Develop Institutional Investor Onboarding Infrastructure

Investor onboarding infrastructure must support KYC, AML, accreditation verification, and institutional identity management within a unified workflow. Financial institutions also require role-based access systems, permission controls, and integrated compliance monitoring to manage private market participation, treasury products, commodity-backed assets, and regulated investment offerings at scale.

- Build Secure Smart Contract and Asset Issuance Systems

Smart contract infrastructure forms the operational layer of institutional RWA platforms. Asset issuers require programmable systems capable of automating issuance, transfer restrictions, coupon distributions, repayment execution, and compliance validation across multiple asset categories. Enterprise-grade development standards, auditability, and contract security become critical requirements when managing high-value financial products and regulated investor environments.

- Integrate Custody, Settlement, and Compliance Operations

Institutional tokenization platforms must integrate digital custody, payment rails, settlement infrastructure, and compliance systems within a single operational framework. Banks and funds require interoperability across core financial operations, including treasury management, reporting, collateral handling, and transaction monitoring. These integrations directly influence scalability, regulatory readiness, and long-term operational efficiency across institutional digital asset ecosystems.

- Enable Secondary Trading and Institutional Scalability

Institutional adoption depends heavily on liquidity access and scalable distribution infrastructure. RWA platforms must support secondary trading capabilities, permissioned investor participation, cross-border accessibility, and multi-asset expansion without compromising compliance controls. Financial institutions are prioritizing platforms capable of supporting long-term product diversification across debt markets, real estate, commodities, private funds, and alternative investment ecosystems.

Wrapping Up

RWA tokenization is positioning digital asset infrastructure as a core layer within institutional finance, treasury operations, and private market distribution. Banks, funds, and asset issuers entering this market early are building long-term advantages across liquidity access, programmable financial products, and global investment participation.

Institutional adoption will depend on secure infrastructure, regulatory alignment, and scalable asset servicing capabilities across multiple jurisdictions and asset classes. Financial institutions prioritizing enterprise-grade RWA tokenization platforms today are positioning themselves for broader participation across digital securities, alternative investments, and tokenized capital markets.

Build RWA Tokenization Platforms for Any Use Case with Shamla Tech Solutions

Shamla Tech Solutions is an RWA tokenization platform development company delivering enterprise-grade infrastructure for banks, funds, asset issuers, and financial institutions across global jurisdictions. Our team develops white-label RWA platforms supporting real estate, private credit, treasury products, commodities, ESG assets, invoice financing, and institutional investment ecosystems.

We provide end-to-end RWA tokenization solutions including asset digitization, smart contract development, investor onboarding, compliance integration, custody infrastructure, secondary marketplace capabilities, and multi-asset issuance frameworks. Our platforms are designed for institutional scalability, regulatory alignment, cross-border operations, and secure digital asset distribution across regulated financial environments.