Cross-border payments continue to impose settlement delays, intermediary costs, fragmented compliance workflows, and limited transaction transparency for global businesses. Stablecoin payment infrastructure offers a practical framework for enterprises seeking programmable settlement, liquidity control, and efficient international value transfer.

By 2026, the global stablecoin market is projected to surpass $400 billion in circulating value, reflecting stronger institutional participation in digital payment infrastructure. This growth highlights the increasing need for stablecoin payment solutions that support faster settlement, cost efficiency, and scalable cross-border transactions.

In this article, we explain how to build a secure stablecoin platform for cross-border payments in the USA, covering platform architecture, essential security controls, regulatory compliance requirements, blockchain infrastructure choices, development stages, and strategic considerations for enterprise-grade payment deployment.

Launch Secure Cross-Border Stablecoin Payment Solutions In USA

Why Are Businesses Building Stablecoin Platforms for Cross-Border Payments in 2026?

Key Business Drivers Behind Enterprise Stablecoin Payment Adoption:

- Cross-border payment delays directly impact enterprise working capital efficiency. Stablecoin platforms enable faster settlement execution, helping businesses reduce idle capital exposure, improve liquidity allocation, and maintain stronger financial predictability across international payment operations.

- Visa’s 2024 annual report says that the company processed $16 trillion in total payments volume, highlighting the scale of global transaction demand. Enterprises are building stablecoin payment infrastructure to capture greater efficiency, automation, and operational control within high-volume payment ecosystems.

- Correspondent banking models create operational complexity through intermediary dependencies, fragmented fee structures, reconciliation delays, and limited transaction visibility. Stablecoin payment platforms provide enterprises with transparent payment execution, auditable transaction records, and stronger governance across international financial operations.

- Modern enterprises require payment infrastructure that supports automated settlements, programmable payout workflows, embedded financial services, and API-driven transaction execution. Stablecoin platforms align with these infrastructure requirements while enabling scalable payment architecture for global business expansion initiatives.

- Enterprises increasingly view payment infrastructure ownership as a strategic commercial advantage. Building proprietary stablecoin platforms enables stronger control over transaction economics, ecosystem participation, customer payment experiences, and long-term monetization opportunities across cross-border financial service operations.

The Growing Need for Faster and Secure Cross-Border Payment Infrastructure

Cross-border payment infrastructure remains commercially inefficient for enterprises managing international settlements, treasury movement, and high-volume disbursements. Stablecoins for cross-border payments address persistent operational friction caused by payment execution delays, fragmented banking dependencies, and limited transaction visibility across global financial workflows.

According to the World Bank, the global average cost of sending $200 internationally remained 6.4%, significantly above the UN Sustainable Development Goal target of 3%, reinforcing the commercial need for more efficient digital payment infrastructure.

Why Existing Cross-Border Payment Infrastructure Falls Short:

- Multi-day settlement cycles restrict working capital efficiency, delaying access to capital that enterprises could otherwise deploy toward supplier payments, treasury optimization, or revenue-generating financial operations.

- Intermediary-led payment routing creates fragmented fee structures, making transaction cost forecasting difficult for enterprises managing recurring international payment volumes across multiple jurisdictions.

- Limited end-to-end transaction visibility creates reconciliation inefficiencies, increasing operational workload for finance teams responsible for payment verification, audit readiness, and exception management.

- Cross-border compliance execution remains operationally intensive, particularly for enterprises navigating AML screening, jurisdiction-specific reporting obligations, and transaction monitoring across stablecoin banking integrations.

Enterprises increasingly require payment infrastructure designed for execution speed, transaction transparency, and stronger operational control at scale.

Core Features of a Stablecoin Platform for Cross-Border Payments

Building a stablecoin platform for cross-border payments requires stablecoin infrastructure that meets enterprise expectations for security, compliance, settlement efficiency, and financial interoperability. The following core features define the technical foundation of a commercially viable stablecoin platform for cross-border payments.

Feature | Key Components | Business Impact |

Multi-Stablecoin Support | USDC, USDT, PYUSD, Fiat-backed enterprise stablecoins | Settlement flexibility across payment corridors |

Enterprise Wallet Infrastructure | MPC custody, Multi-signature approvals, Role-based access, HSM security | Secure treasury control and governed fund movement |

Compliance Engine | KYC verification, AML screening, OFAC checks, SAR monitoring | Regulatory compliance and lower operational risk |

Fiat Integration Layer | ACH, SWIFT, SEPA, Wire transfers, Banking APIs | Seamless fiat on/off-ramp execution |

Settlement Engine | Ethereum, Stellar, Solana, Polygon, Private blockchain rails | Faster international payment execution |

Risk Monitoring System | Fraud analytics, Transaction monitoring, Audit logs, Anomaly detection | Real-time payment oversight and fraud prevention |

Enterprise API Integration | SAP, Oracle NetSuite, Salesforce, Payroll APIs, Treasury systems | Automated reconciliation and payment orchestration |

1. Multi-Stablecoin Settlement Support

2. Institutional Wallet and Treasury Management

3. Embedded KYC, AML, and Sanctions Compliance

4. Fiat Banking and Liquidity Integration

5. Real-Time Cross-Border Settlement Engine

6. Transaction Monitoring, Audit Trails, and Risk Intelligence

7. API and Enterprise System Integration

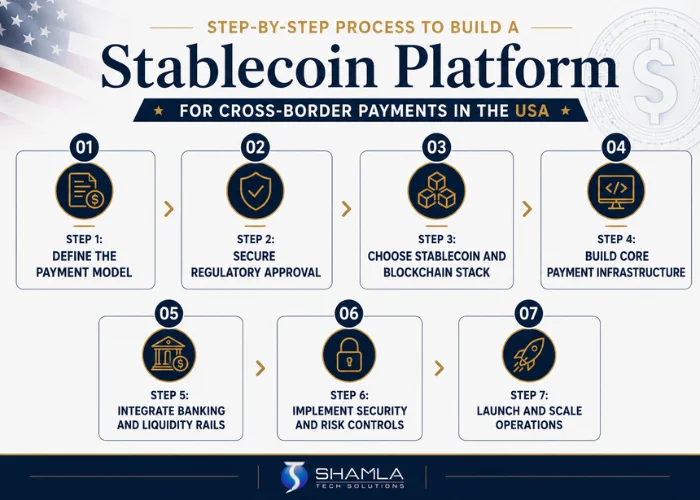

Step-by-Step Process to Build a Stablecoin Platform for Cross-Border Payments in the USA

Step 1: Define the Commercial Payment Use Case

Step 2: Establish U.S. Regulatory and Compliance Requirements

Step 3: Select the Stablecoin and Blockchain Infrastructure

Step 4: Build the Core Payment Infrastructure

Step 5: Integrate Banking Rails and Liquidity Infrastructure

Step 6: Implement Security and Risk Governance Controls

Step 7: Launch, Optimize, and Scale Payment Operations

Build Enterprise-Grade Stablecoin Payment Infrastructure For Global Growth

Security and Compliance Requirements for Stablecoin Payment Platforms in USA

FinCEN, SEC, and Licensing Compliance

KYC, AML, and Sanctions Enforcement

Institutional Security Architecture

Smart Contract and Operational Risk Management

Best Blockchain Networks for Cross-Border Stablecoin Payment Development

Blockchain infrastructure determines how efficiently a stablecoin payment platform handles settlement execution, transaction costs, interoperability, and scalability. Selecting the right network requires balancing enterprise payment requirements, compliance expectations, and commercial performance across international transaction corridors.

Blockchain Network | Best Fit for Cross-Border Payments | Key Strengths | Enterprise Consideration |

Ethereum | High-value institutional settlements | Deep USDC ecosystem, institutional adoption, strong smart contract infrastructure | Higher gas fees during congestion |

Stellar | Remittances, payment corridors, settlement networks | Fast settlement, low transaction costs, payment-focused architecture | Limited smart contract flexibility compared to broader ecosystems |

Solana | High-volume transaction processing | Extremely fast settlement, low fees, strong scalability | Enterprise adoption still maturing |

Polygon | Cost-efficient enterprise payment infrastructure | Ethereum compatibility, low transaction fees, scalable execution | Dependency on Ethereum ecosystem assumptions |

XRP Ledger | Cross-border liquidity and financial settlement | Banking-focused design, efficient international settlement, strong transaction throughput | Regulatory perception considerations in certain markets |

Hyperledger Besu (Permissioned) | Regulated enterprise financial infrastructure | Controlled governance, privacy, compliance flexibility, institutional architecture | Lower interoperability with public blockchain ecosystems |

The most suitable blockchain depends on settlement volume, transaction economics, regulatory expectations, and interoperability requirements. Enterprise stablecoin payment platforms perform best when blockchain infrastructure aligns with commercial payment execution priorities, rather than relying solely on transaction speed or network popularity.

Business Benefits of Stablecoin-Based Cross-Border Payment Platforms

Faster Settlement and Treasury Liquidity Optimization

Reduced Payment Processing and FX Cost Exposure

Stronger Payment Traceability and Audit Governance

Automated Global Payment Operations

Scalable International Payment Infrastructure Ownership

Challenges in Stablecoin Platform Development for Cross-Border Payments

Regulatory Complexity Across Jurisdictions

Banking and Liquidity Integration Challenges

Security and Operational Risk Exposure

Scalability and Enterprise Infrastructure Complexity

Wrapping Up

Cross-border payments are becoming a strategic infrastructure decision rather than a back-office financial function. Enterprises that invest in stablecoin payment capabilities today position themselves for stronger settlement control, improved treasury efficiency, and greater ownership over how international value moves.

Building this infrastructure requires disciplined execution across compliance, security, banking interoperability, and payment architecture. Businesses entering this space with a long-term commercial mindset will be better positioned to establish differentiated payment capabilities in an increasingly competitive global financial environment.

Build Stablecoin Platform for Cross-Border Payments with Shamla Tech Solutions

Shamla Tech Solutions is a stablecoin development company delivering enterprise-grade platforms for cross-border payments in the USA. Our expertise spans stablecoin architecture, wallet infrastructure, compliance-ready payment systems, banking integrations, and secure blockchain development tailored for regulated international payment operations.

From USDC and USDT payment platforms to custom stablecoin ecosystems, Shamla Tech Solutions helps businesses build scalable cross-border payment infrastructure aligned with U.S. compliance expectations. We develop secure, interoperable solutions engineered for treasury efficiency, transaction transparency, and enterprise financial performance.

Transform International Payments With Custom Stablecoin Platform Development

FAQs

1. What is a stablecoin platform for cross-border payments?

2. How much does it cost to build a stablecoin platform for cross-border payments?

3. Which blockchain is best for cross-border stablecoin payment development?

4. Are stablecoin payment platforms legal in the United States?

5. Why should businesses partner with a stablecoin development company?

Building enterprise-grade stablecoin payment infrastructure requires expertise in blockchain engineering, compliance architecture, banking integrations, wallet security, and transaction governance. Specialized development partners help businesses reduce implementation risk and accelerate commercial deployment timelines.