Private credit is debt financing offered by non-bank lenders. Examples include direct loans to mid-sized firms, real estate loans, or consumer loans. This debt is not issued as a marketable bond on public markets. Private credit has become an asset class of more than $2 trillion globally over the previous decade, partly due to investment funds (private equity companies, credit funds) filling the gap left by banks after 2008. Loans are generally illiquid; a fund tends to hold the loan until maturity as there is no known exchange where a fraction of a private loan may be readily sold (other than customized secondary sales, which are slow and need due diligence on the part of the buyer).

Private credit arrangements are typically between a lead arranger and the borrower, with conditions agreed on a case-by-case basis and the documentation kept secret. Private credit’s higher risk and illiquidity mean that rates are generally higher than public market rates, making private credit appealing to yield-seeking investors. But because they are not traded on a public market, transparency is poor and only institutional or accredited investors (with large minimums that can exceed $5 million) can normally invest. This structure has allowed private lending to offer better rates than leveraged loans and high-yield bonds to depositors.

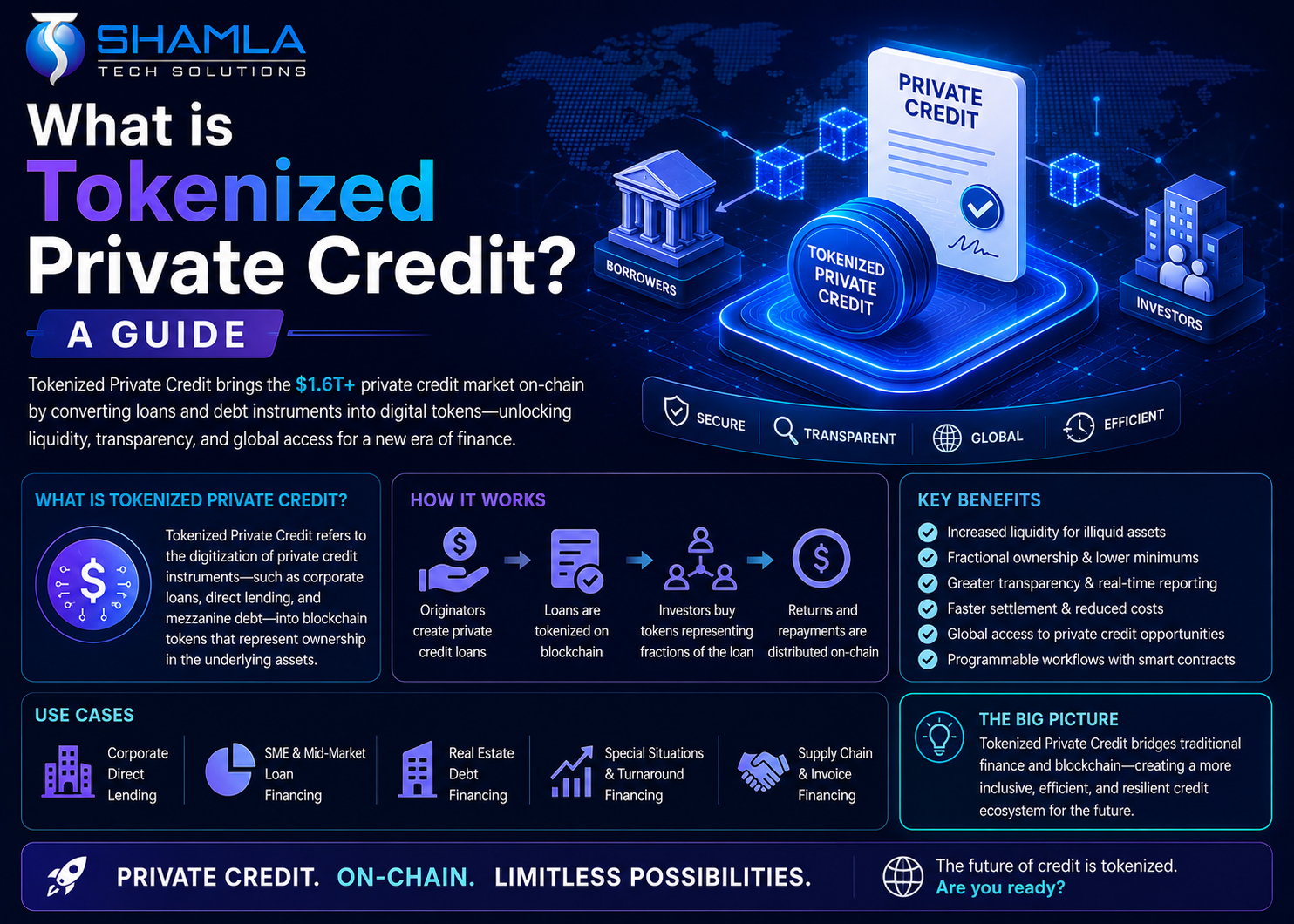

Why do we need Tokenized Private Credit?

Illiquidity: As a held to maturity investment, if a lender desires to exit early, there is no deep market of buyers quoting prices immediately. Sales are often discounted and require the approval of the borrower or agent, which can take weeks to months. Investors require a “illiquidity premium” – more yield as compensation for being stuck.

High Minimums / Limited Access: Private loans typically need big minimum investments, therefore many funds only accept pledges of $5–10 million or more.

Lack of Transparency & Price Discovery: There is no public market, therefore loan values are not updated regularly (typically quarterly) and are based on subjective models or broker quotes, making it difficult to assess the fair value of a loan until an event such as a default or an acquisition occurs.

Private credit markets have long been subject to rigorous securities laws established for private placements. Traditionally, private credit funds and direct lending arrangements in the U.S. were issued under exemptions such as Regulation D, limiting the pool of investors to qualified individuals or institutions on the theory that such investors could take care of themselves without the full panoply of registration safeguards. These investments were very illiquid, featuring multi-year lockups and significantly less disclosure requirements than public offerings. Similar regimes existed in the EU where offers to the public generally needed a prospectus or were subject to limited private placement exemptions.

This regulatory environment presents serious challenges to democratizing access to private lending. U.S. securities regulation traditionally limits non-accredited investors from most private credit options, and EU regulations like as MiFID II have similar restrictions, with the aim of protecting retail investors. These regulations are protective yet limit participation to the rich or institutional players. Cross-border offerings also create jurisdictional issues because companies generally must comply with the rules in each market in which they are providing investments.

The Future of Tokenized Private Credit

Private credit is a perfect fit between the basic value proposition of bitcoin and traditional finance. This industry democratizes access to financing and fundraising, enabling permissionless 24/7 marketplaces that overcome traditional liquidity limits. The historical worry regarding the enforcement mechanisms of defaults and liquidations are increasingly being answered, giving a more robust framework for the engagement of institutions. Private credit protocols with ~$12.2B current TVL and proven product-market fit have shown the technological and operational viability of this business.

Unlike prior sectors that focused on crypto-native tokens, private credit onchain has primarily drawn traditional finance participants. For example, non-crypto natives use Tradable and much of the TVL in this arena comes from TradFi data being integrated onchain. But onchain markets like Maple are still around 50x smaller than Aave’s markets, while giving better payouts to lenders.

Private Credit vs Tokenized Private Credit

Feature | Traditional Private Credit | Tokenized Private Credit |

Liquidity | Illiquid, held until maturity | Improved liquidity via secondary markets |

Minimum Investment | High ($5M+ typical) | Fractional ownership enables smaller investments |

Accessibility | Limited to institutional/accredited investors | Broader access (global investors, DAOs, family offices) |

Transparency | Low, periodic reporting (quarterly) | High, real-time onchain data visibility |

Price Discovery | Difficult, model-based valuations | Continuous market-driven pricing |

Compliance | Manual, document-heavy processes | Automated via smart contracts (KYC/AML, rules) |

Settlement Speed | Slow (days to months) | Faster, near-instant blockchain settlement |

Interoperability | Siloed systems | Integrated with DeFi and digital ecosystems |

Operational Efficiency | High manual overhead | Automated processes reduce costs |

Institutional Adoption and Future Outlook

At the end of the decade, private credit will be a big part of the expected trillions of dollars of tokenized real-world assets. “We’re seeing large asset managers move from proof-of-concept pilots into production-grade deployments.

Industry leaders are already issuing digital bonds and tokenizing money market products using blockchain. Onchain financing is now funding real-world firms, with Ondo Finance, Centrifuge and others showcasing the potential of this new paradigm and giant institutions like BlackRock joining the area with tokenized funds. These developments are a hint that tokenized credit is no longer theoretical. It is a constantly rising segment of the financial economy.

As usage grows, so does the need for standardized data and interoperability. Shamlatech builds the industry standard oracle platform that is bringing the capital markets onchain and powering the majority of decentralized finance (DeFi).

Tokenization of Private Credit: Use Cases & Advantages

Traditionally private credit investments like SME loans, trade financing or structured credit have been reserved for large institutions.

Tokenization solves this problem by breaking these securities into smaller, tradeable units, allowing a wider base of investors to participate, such as family offices, accredited investors, DAOs and overseas investors. Interoperable token standards allow financial items to travel between systems as tokens easily.

Private lending has traditionally been illiquid and typically has extensive lock-up periods.

Tokenization represents debt as digital tokens that can trade on compliant secondary markets, opening up future liquidity and price discovery. Investors can trade fractions of loans onchain, and tokens can be merged, tranched or wrapped into new products such as stablecoin-backed yield instruments or DeFi lending pools.

Tokenization also helps handle major compliance and regulatory concerns.

Investor records are private, traceable and auditable using onchain identities, validated credentials and KYC/AML systems on blockchain. Smart contracts implement regulatory duties like as whitelisting, transfer limitations, and jurisdictional rules directly onto the tokens, replacing document-heavy, post-trade verification.

Data fragmentation has long hampered openness and valuation in private finance.

One source of truth regarding loan terms, performance, ownership and investment positions, accessible to authorized parties, comes from onchain records. Quarterly reporting is replaced by real-time updates, decreasing operational risk and providing for continuous monitoring, correct valuations, benchmarking and richer analytics.

Tokenized Private Credit: Popular Use-Cases

- Maple Finance

Built on Ethereum and Solana, Maple facilitates tokenized corporate credit. Lenders deploy capital into “pools” managed by delegates who underwrite deals.

- Centrifuge

Centrifuge allows real-world assets (like invoices or real estate debt) to be tokenized and financed through the Tinlake protocol.

- Securitize

Securitize focuses on compliance-first infrastructure. Its platform tokenizes private equity, venture funds, and credit products for firms like KKR.

Conclusion

Private credit has long been a powerful but restricted asset class—dominated by institutions, limited by illiquidity, and constrained by high entry barriers. As highlighted in your content, the traditional system suffers from lack of transparency, poor price discovery, and limited accessibility, making it difficult for broader participation .

Tokenization is fundamentally changing this landscape.

By bringing private credit onchain, tokenization introduces:

- Fractional ownership

- Real-time transparency

- Secondary market liquidity

- Automated compliance

This shift is not theoretical anymore. With increasing institutional adoption and billions already flowing into tokenized credit markets, the future of private lending is clearly digital, decentralized, and accessible.

However, unlocking this potential requires robust infrastructure, regulatory alignment, and seamless integration between traditional finance and blockchain systems.

That’s where the right technology partner becomes critical.

What Does Shamlatech Offer as the Best Private Credit Tokenization Platform Development?

Shamlatech stands out as a leading provider of end-to-end private credit tokenization solutions, enabling financial institutions, asset managers, and enterprises to seamlessly transition into onchain finance.

End-to-End Tokenization Infrastructure

Compliance-First Architecture

Built with global regulatory frameworks in mind, the platform integrates:

- KYC/AML verification

- Investor whitelisting

- Jurisdiction-based transfer restrictions

This ensures that tokenized assets remain fully compliant across regions.

Advanced Smart Contract Automation

Smart contracts automate:

- Interest payments

- Loan servicing

- Investor distributions

- Compliance enforcement

Reducing operational overhead and minimizing manual intervention.

Liquidity Enablement & Secondary Markets

Real-Time Data & Transparency

Unlike traditional quarterly reporting, Shamlatech offers:

- Onchain data visibility

- Real-time performance tracking

- Improved valuation and analytics

Interoperability & DeFi Integration

Assets can be:

- Integrated with DeFi protocols

- Used as collateral

- Structured into new financial products

Scalable & Customizable Solutions

Whether for:

- SME lending

- Trade finance

- Structured credit

Shamlatech delivers tailored solutions aligned with business and regulatory needs.

FAQs

1. What is tokenized private credit?

2. Why is tokenization important for private credit markets?

Traditional private credit markets are illiquid, opaque, and limited to large investors. Tokenization solves these issues by enabling:

- Liquidity through secondary trading

- Broader investor access

- Real-time data and transparency

3. Who can benefit from tokenized private credit?

- Asset managers

- Institutional investors

- Family offices

- DAOs

- Accredited and global investors

4. How does tokenization ensure regulatory compliance?

Through blockchain-based systems such as:

- Onchain identity verification

- KYC/AML integration

- Smart contract-enforced transfer restrictions

These automate compliance while maintaining transparency and auditability .

5. Why choose Shamlatech for private credit tokenization?

Shamlatech combines:

- Deep blockchain expertise

- Compliance-first architecture

- End-to-end infrastructure

- Scalability and customization

making it a reliable partner for building secure, compliant, and future-ready tokenized private credit platforms.