Cross-border B2B payments sit at the center of global commerce, yet finance leaders continue to scrutinize how capital moves between counterparties. Settlement speed, liquidity utilization, transaction visibility, and treasury efficiency now carry greater weight in payment infrastructure decisions.

The global cross-border payments market is projected to exceed $290 trillion in annual transaction value by 2030, reflecting the scale of enterprise payment activity. As transaction volumes increase, organizations are prioritizing payment mechanisms that support predictable settlement and improved operational control.

This article examines B2B stablecoin payments vs SWIFT, including how each system functions, the differences in settlement processes, transaction costs, transparency, and treasury management considerations. We also explore why finance teams are evaluating stablecoin-based payment infrastructure for business transactions.

Build Faster Cross-Border Payment Infrastructure

What Are B2B Stablecoin Payments and How Do They Work?

Key Operational Characteristics of B2B Stablecoin Payments:

- Businesses issue payments using stablecoins pegged to fiat currencies such as the US dollar, allowing counterparties to receive funds without exposure to the price volatility commonly associated with digital assets or speculative cryptocurrency markets.

- Settlement occurs directly through blockchain infrastructure, enabling payment execution independent of correspondent banking layers. This structure supports continuous transaction availability, giving finance teams greater flexibility when managing global vendor obligations and treasury operations.

- Stablecoin payment workflows can be integrated into ERP, invoicing, and treasury systems, creating a more connected financial environment where payment initiation, reconciliation, and transaction verification are recorded through a unified operational framework.

- Stablecoin transaction volume exceeded $33 trillion in 2025, highlighting growing institutional participation across payments, settlements, treasury movements, and cross-border transfers. The scale reflects increasing enterprise interest in blockchain-based payment infrastructure for commercial transactions.

- Payment visibility is recorded on-chain, allowing finance teams to monitor transaction status, confirm settlement activity, and maintain audit-ready payment records. This level of transparency supports stronger financial controls across multi-entity and cross-border business operations.

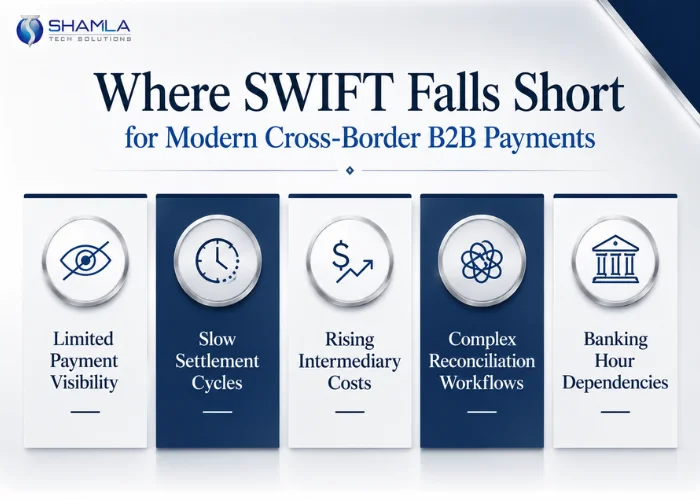

Where SWIFT Falls Short for Modern Cross-Border B2B Payments

1. Limited End-To-End Payment Visibility

2. Settlement Timelines That Impact Working Capital

3. Intermediary Banking Costs That Reduce Payment Efficiency

4. Reconciliation Processes That Increase Operational Overhead

5. Dependence On Banking Hours And Regional Cut-Off Times

B2B Stablecoin Payments vs SWIFT: Key Differences in Speed, Cost, Transparency, and Settlement

As finance teams evaluate payment infrastructure, the discussion increasingly centers on operational efficiency rather than payment initiation alone. Settlement timelines, transaction costs, liquidity utilization, and payment visibility have become critical considerations for organizations managing global supplier networks and cross-border payment flows.

Factor | B2B Stablecoin Payments | SWIFT Payments |

Settlement Speed | Seconds to minutes | Typically 1-5 business days |

Transaction Availability | 24/7/365 | Dependent on banking hours and cut-off times |

Payment Visibility | Real-time on-chain tracking | Limited end-to-end visibility |

Intermediaries | Direct blockchain settlement | Multiple correspondent banks may be involved |

Transaction Costs | Often a few cents to a few dollars | Can range from $15-$50+ per transaction, excluding FX spreads |

Liquidity Efficiency | Near-instant settlement | Capital may remain in transit for days |

Reconciliation | Shared transaction records | Multiple systems and institutions involved |

Global Accessibility | Network-based participation | Banking infrastructure dependent |

Faster Settlement Improves Capital Efficiency

Lower Transaction Costs Support Margin Preservation

Real-Time Visibility Strengthens Financial Control

Continuous Settlement Eliminates Operational Delays

Modernize International B2B Payment Operations Efficiently

Add Your Heading Why Finance Teams Are Exploring Stablecoin-Based Payment InfrastructureHere

Greater Control Over Global Liquidity

Reduced Dependence on Complex Banking Networks

Improved Visibility Across Payment Operations

Infrastructure Better Aligned With Global Business Activity

Bottom Line

Cross-border payments are no longer evaluated solely on reliability. Finance leaders are increasingly examining how payment infrastructure affects liquidity, operational efficiency, and treasury performance. This shift is bringing stablecoin-based payment networks into discussions that were historically dominated by traditional banking and SWIFT-based workflows.

For organizations managing international payments at scale, stablecoins introduce capabilities that align more closely with modern treasury requirements, including faster settlement, continuous transaction availability, and greater payment visibility. As adoption expands across enterprise finance, stablecoin-based payment infrastructure is becoming an increasingly relevant consideration for cross-border B2B transactions.

Build B2B Stablecoin Payment Solution with Shamla Tech Solutions

Shamla Tech Solutions is a stablecoin development company specializing in enterprise-grade payment infrastructure for cross-border business transactions. We design and develop secure stablecoin payment solutions with support for treasury operations, invoicing workflows, settlement automation, and multi-currency transaction environments across global jurisdictions.

Our team delivers end-to-end stablecoin payment platforms tailored to business requirements, regulatory considerations, and operational objectives. From wallet infrastructure and payment gateways to compliance integrations and settlement management, we help organizations build scalable payment ecosystems capable of supporting international B2B transaction volumes.