The GENIUS Act establishes a regulatory framework for bank-issued stablecoins within existing supervisory regimes. It defines how stablecoins issued by regulated banks are structured, backed, governed, and redeemed, placing them within the scope of regulated financial operations.

The Act sets explicit requirements for reserve backing, redemption assurance, governance, and oversight. Stablecoin issuance by banks is evaluated using the same standards applied to payments, settlement, and liquidity functions. Regulatory compliance is enforced through system design rather than addressed through policy alone.

This article outlines the implications of the GENIUS Act for bank-issued stablecoin infrastructure. We cover the operational and architectural requirements banks and financial institutions must address to issue stablecoins under supervisory oversight, including issuance controls, reserve management, transparency, and reporting.

The GENIUS Act: What It Establishes for Bank-Issued Stablecoins

The enactment of the GENIUS Act established a federal regulatory framework for stablecoins in the United States, providing banks with defined conditions for issuance and operation. Following this regulatory alignment, stablecoin adoption accelerated sharply, with total stablecoin market capitalization increasing by 49% in 2025. This growth reflects increased participation by regulated financial institutions and positions bank-issued stablecoins within existing supervisory regimes.

For banks, the GENIUS Act converts stablecoin issuance into a regulated financial operation governed by the same supervisory expectations applied to payments, settlement, and liquidity infrastructure. Stablecoins issued by banks are evaluated based on how issuance, reserve management, redemption, and reporting are enforced at the system level.

From a stablecoin development perspective, the Act introduces clear constraints that shape stablecoin platform design and operating models:

- Reserve-enforced issuance models: Stablecoin supply must be tied directly to verified reserves held under the issuing bank’s control. Platform architecture must enforce one-to-one backing through deterministic issuance logic and real-time reserve reconciliation.

- Redemption-driven liquidity workflows: Redemption at par is a core obligation. Systems must support predictable redemption execution, liquidity availability, and operational continuity under stressed conditions.

- Controlled mint and burn operations: Issuance and destruction of stablecoins are treated as regulated banking actions. Platforms must implement strict authorization controls, segregation of duties, and full audit trails across all mint and burn events.

- Supervisory visibility by design: Regulators require continuous access to issuance volumes, reserve balances, and operational activity. Reporting pipelines must be structured, auditable, and aligned with existing regulatory disclosures.

- Institutional governance enforcement: Stablecoin programs operate within a bank’s governance, risk, and compliance framework. Platform controls must support accountability, exception handling, and supervisory review without manual intervention.

Together, these requirements define bank-issued stablecoins as regulated financial instruments supported by banking-grade infrastructure. Compliance depends on platforms that translate regulatory expectations into enforceable system controls across issuance, reserves, redemption, and reporting.

GENIUS Act as a Catalyst for Institutional Stablecoin Adoption

The GENIUS Act changes how stablecoin initiatives are approved, funded, and governed inside financial institutions. By anchoring stablecoin issuance within existing supervisory structures, the Act allows banks to route stablecoin programs through established approval paths used for payments, treasury systems, and settlement infrastructure.

This shifts stablecoin initiatives out of isolated innovation tracks and into core operating budgets, risk committees, and production deployment cycles, materially accelerating execution timelines for institutions prepared to operate under regulatory oversight.

Institutional Adoption Signals in 2025

- JPMorgan Chase continued expansion of JPM Coin for interbank settlement, demonstrating sustained use of bank-issued stablecoins within regulated treasury and liquidity operations.

- Société Générale advanced issuance of USD CoinVertible, marking one of the first publicly disclosed dollar-denominated stablecoins issued by a major European bank under a regulated framework.

- BNP Paribas, ING, and UniCredit participated in a consortium exploring euro-denominated stablecoin issuance, signaling coordinated institutional engagement across European banking markets.

- Visa expanded stablecoin settlement capabilities using USDC, enabling regulated institutions to settle transactions over stablecoin rails within established payment networks.

Intersection of Stablecoin Adoption and System Readiness

Institutional adoption under the GENIUS Act converges with execution capability. As stablecoin initiatives move into regulated operating environments, adoption decisions become inseparable from the ability to sustain issuance, settlement, and reporting under supervisory scrutiny. Stablecoins adopted by financial institutions must operate as durable components of regulated financial infrastructure, where scale, control, and reliability determine long-term viability.

Why Bank-Issued Stablecoins Are Treated Differently Under the GENIUS Act

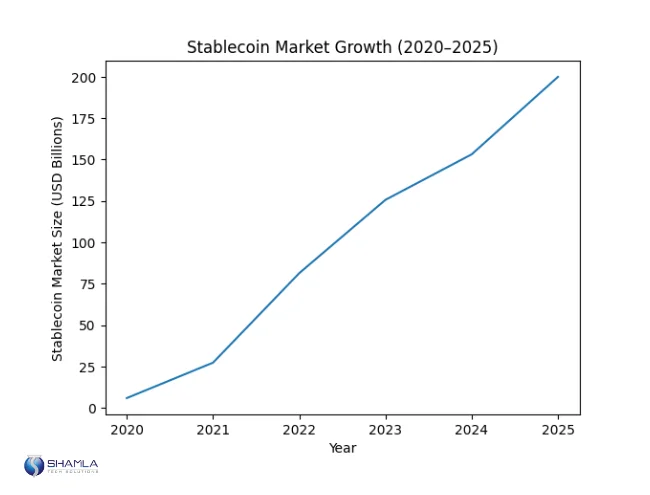

Regulatory focus intensified as stablecoin usage scaled from approximately $5.9 billion in 2020 to $200 billion by 2025, increasing the systemic relevance of stablecoin issuance. At this scale, regulators prioritize issuer accountability, balance-sheet integrity, and enforceable redemption obligations. Banks meet these criteria through established prudential oversight rather than newly created regulatory constructs.

Several factors explain why bank-issued stablecoins receive distinct treatment under the Act:

- Supervised custody of customer funds: Banks already manage customer deposits under strict custody, segregation, and reporting rules. This allows stablecoin reserves to be held, monitored, and examined within existing supervisory structures.

- Balance-sheet accountability: Bank-issued stablecoins are evaluated as obligations of the issuing institution. This ties issuance directly to capital, liquidity, and risk management standards that do not apply to non-bank issuers.

- Enforceable redemption responsibility: Banks are legally obligated to honor customer claims. This enables redemption guarantees to be enforced through supervisory and resolution frameworks rather than contractual assurances alone.

- Established governance and examination cycles: Banks undergo regular regulatory examinations. Stablecoin programs issued by banks fall within these cycles, allowing regulators to assess controls, exceptions, and operational practices on an ongoing basis.

- Integration with regulated payment activity: Stablecoins issued by banks align with payment, settlement, and treasury functions already subject to oversight. This reduces reliance on parallel regulatory regimes for digital assets.

These characteristics allow regulators to treat bank-issued stablecoins as regulated financial instruments supported by existing institutional controls. The distinction is based on issuer accountability and supervisory reach, not market share or technology choice.

Infrastructure Implications for Banks Issuing Stablecoins

The GENIUS Act applies supervisory expectations to bank-issued stablecoins that directly affect how issuance, reserves, redemption, and reporting are supported at the system level. Stablecoin operations are evaluated alongside other regulated banking functions, making infrastructure design and operational reliability central to compliance.

For banks, these expectations translate into specific infrastructure implications that determine whether stablecoin issuance can operate at scale under supervisory oversight.

Infrastructure Implications of GENIUS Act Requirements

Stablecoin Function | Infrastructure Implication for Banks |

Issuance and supply control | Systems must enforce authorized mint and burn workflows with immutable traceability and role-based access controls |

Reserve management | Infrastructure must maintain continuous synchronization between outstanding supply and verified reserve balances, with audit-ready records |

Redemption processing | Systems must support predictable, high-availability redemption flows backed by real-time liquidity visibility |

Supervisory reporting | Data pipelines must produce structured, repeatable reporting aligned with regulatory examination requirements |

Governance enforcement | Change management, approvals, and exception handling must align with institutional governance frameworks |

Operational resilience | Stablecoin services must meet availability, recovery, and incident-response standards applied to critical banking systems |

Operational Impact for Banks

These infrastructure requirements place stablecoin issuance within the same operational tier as payments, settlement, and treasury systems. Manual reconciliation, periodic reporting, or discretionary controls are insufficient at this level of supervisory scrutiny.

Banks issuing stablecoins must demonstrate that core stablecoin functions continue to operate with accuracy, control, and availability during peak demand, supervisory review, and operational stress.

Designing GENIUS-Ready Stablecoin Platforms

The GENIUS Act establishes requirements that are enforced through system behavior, not documentation. Stablecoin platforms supporting bank-issued issuance must translate regulatory expectations into controls that operate continuously across issuance, reserves, redemption, and reporting.

GENIUS-ready stablecoin platforms are defined by how reliably they enforce constraints under scale, supervisory review, and operational stress. Design decisions determine whether compliance remains consistent over time or degrades as usage increases.

Key stablecoin design considerations include the following:

Issuance and Supply Governance

Reserve Alignment and Verification

Redemption Reliability

Supervisory Transparency and Reporting

Governance, Control, and Change Management

Resilience and Continuity

Design Outcome

Stablecoin Infrastructure Becomes Banking Infrastructure

The GENIUS Act brings stablecoin issuance under defined banking supervision by setting enforceable requirements around reserves, redemption, governance, and oversight. For bank-issued stablecoins, this establishes clear conditions for how issuance is approved, how obligations are honored, and how operations are examined over time.

Under this framework, infrastructure quality becomes the primary differentiator. Stablecoin systems are judged on their ability to maintain issuance control, reserve alignment, redemption reliability, and supervisory transparency as usage scales. These characteristics determine whether stablecoin operations can withstand regulatory review and sustained institutional use.

Looking ahead, banks engaging with stablecoins will prioritize systems built for longevity. Stablecoin operations must scale without weakening controls, adapt to evolving supervisory expectations, and remain reliable across market cycles. Stablecoins that succeed will function as durable components of regulated banking infrastructure, supported by systems designed for long-term operation rather than short-term deployment.

Build Bank-Grade Stablecoin Infrastructure With Shamla Tech

Bank-issued stablecoins operate under supervisory expectations that extend across issuance control, reserve integrity, redemption reliability, and ongoing regulatory visibility. Meeting these requirements depends on systems designed to function within regulated banking environments from the outset.

Shamla Tech is a stablecoin development company working with banks and financial institutions to design and implement stablecoin platforms aligned with regulatory frameworks such as the GENIUS Act. We build systems that support controlled issuance, continuous reserve alignment, reliable redemption workflows, and audit-ready reporting, while maintaining scalability and operational resilience.

For institutions preparing to issue or adopt stablecoins, long-term success depends on infrastructure that can sustain regulatory scrutiny as volumes increase and oversight intensifies. Shamla Tech supports this transition by delivering stablecoin platforms built for compliance, durability, and sustained operation within regulated financial ecosystems.

Contact us to build bank-grade stablecoin infrastructure aligned with the GENIUS Act.