Rain, the stablecoin payments infrastructure company, reached a $1.95 billion valuation in the beginning of 2026, at a time when capital allocation in digital assets has become far more selective. Valuations at this level are not driven by user growth narratives or speculative potential, but by the perceived durability of the underlying infrastructure.

The valuation reflects growing confidence in stablecoin payments as a practical settlement layer rather than a niche crypto use case. Rain’s integration with established payment networks, including Visa, highlights how stablecoin rails are being aligned with existing financial systems rather than positioned as an alternative to them.

This article examines what Rain’s valuation signals for the stablecoin payments market, the infrastructure model behind such platforms, how similar payment stacks can be built today, and what industry leaders should expect as stablecoin-based payments become part of standard financial operations.

Build a stablecoin payment platform designed for real-world scale

Rain Hits $1.95B: What This Valuation Actually Means for Stablecoin Payments

What this valuation signals:

- Stablecoin payments are being designed as settlement rails that operate continuously and at scale. This places emphasis on uptime, reconciliation, and failure handling as core system requirements.

- Integration with existing payment ecosystems is expected. Stablecoin infrastructure is being connected to Visa-linked card networks, merchant acquiring systems, and enterprise payment operations to support real-world acceptance.

- Compliance is embedded directly into payment flows. Identity, transaction controls, and jurisdiction rules are enforced as part of the transaction lifecycle.

- Payment infrastructure is being built for sustained activity such as card spend, payouts, and treasury movements. These flows require consistent performance and operational clarity.

- Stablecoin payment stacks are converging on a common structure that combines on-chain settlement, abstraction layers for usability, and interfaces aligned with enterprise finance teams.

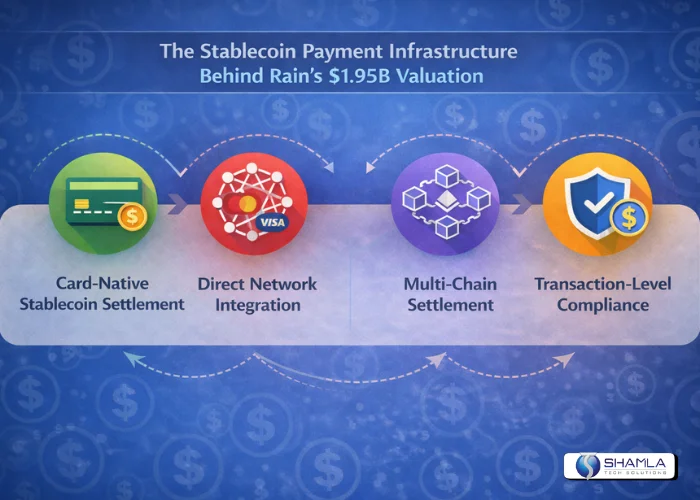

The Stablecoin Payment Infrastructure Behind Rain’s $1.95B Valuation

Card-Native Stablecoin Settlement Built for Real Spend

Rain’s infrastructure is designed around card issuance and card acceptance, not generic token transfers. Stablecoin balances settle on-chain, but authorization, clearing, and merchant interaction follow card network logic.

This alignment matters because card payments impose strict expectations around latency, reversals, and guarantees. By meeting those constraints, the system fits directly into existing global spending behavior, allowing stablecoins to function in everyday payment contexts without altering how merchants or consumers operate.

Direct Network-Level Integration Instead of Layered Intermediaries

Rain operates at the card network level rather than relying on multiple processors or aggregators. This gives tighter control over issuance, settlement coordination, and compliance obligations. Fewer intermediaries reduce operational risk and improve predictability at scale.

In payments infrastructure, this kind of positioning signals durability. It allows the platform to grow payment volume without introducing fragility from dependency chains that often break under regulatory or operational pressure

Multi-Chain Settlement Driven by Payment Economics

Rain treats blockchains as settlement components selected based on cost, speed, and reliability. The choice of chain is routed by payment requirements, not ecosystem loyalty. This approach keeps transaction costs manageable while meeting performance expectations tied to card usage.

Over time, this flexibility supports higher volumes and broader geographic reach. The infrastructure reflects a payments mindset where efficiency and consistency matter more than protocol identity.

Transaction-Level Compliance Embedded Into Card and Wallet Controls

Compliance is enforced before settlement through permissioning tied to card issuance and wallet activity. Identity, jurisdiction rules, and transaction limits operate as execution constraints rather than monitoring layers applied after the fact.

This reduces downstream risk and simplifies regulatory alignment as volumes increase. For payment systems connected to global card networks, this structure enables expansion without repeatedly reworking compliance logic as new markets and use cases are added.

Building a Stablecoin Payment Infrastructure That Operates at Global Scale

Layer | What It Needs to Solve | Why It Matters at Scale |

Settlement | Consistent, fast value movement | Payments cannot pause or degrade |

Payment Integration | Compatibility with global systems | Merchants won’t change workflows |

Compliance | Rule enforcement inside transactions | Manual controls do not scale |

Chain Strategy | Cost and performance optimization | Fees and latency compound quickly |

Operations | Visibility and control for teams | Finance teams need clarity |

1. Settlement Architecture Designed for Continuous Use

A global stablecoin payment system must behave like financial infrastructure, not like an application. Settlement cannot depend on manual intervention, variable confirmation assumptions, or best-effort processing. The system should handle retries, partial failures, and reconciliation automatically.

Payment state must be clear at every step, especially when bridging on-chain settlement with off-chain records. At scale, most issues come from edge cases, not happy paths. Designing for continuous operation means accepting that failures will happen and ensuring the system absorbs them without interrupting payment flows.

2. Deep Integration With Existing Payment and Merchant Systems

Global adoption depends on compatibility with how payments already work. Stablecoin infrastructure must plug into card networks, merchant acquiring systems, and enterprise finance tools without forcing operational changes. Merchants expect authorization, clearing, refunds, and reporting to behave consistently.

Finance teams expect familiar settlement files and reconciliation processes. When stablecoin payments fit inside these expectations, adoption accelerates. When they do not, they stall. The infrastructure layer must absorb blockchain complexity so that downstream systems continue to operate as they always have.

3. Compliance Embedded Into Transaction Execution

Compliance cannot sit outside the payment system when operating globally. Identity checks, transaction limits, jurisdiction rules, and monitoring must be enforced before value moves. This reduces downstream risk and avoids operational bottlenecks.

Embedding compliance into execution allows payments to scale without adding manual review layers as volume grows. It also supports expansion into new regions without redesigning the entire system. At scale, compliance becomes a systems engineering problem. Solving it early prevents slowdowns, regulatory friction, and inconsistent enforcement later.

4. Chain Selection Driven by Payment Economics

Stablecoin payment infrastructure should treat blockchains as interchangeable settlement layers. Each chain has different cost, speed, and reliability characteristics. Routing payments based on these properties keeps fees predictable and performance consistent as volume increases.

Locking the system to a single chain introduces risk when network conditions change. A payment-first chain strategy prioritizes throughput, finality behavior, and operational stability. This flexibility allows the infrastructure to adapt as usage grows and as blockchain networks evolve, without disrupting payment operations.

5. Operational Visibility Built for Finance and Payments Teams

Global payment systems live or die by operational clarity. Teams need real-time visibility into balances, settlement status, exceptions, and reconciliation outcomes. Stablecoin infrastructure should expose this information in formats finance and operations teams understand.

Internal users should not need blockchain expertise to manage payments. Clear reporting, audit trails, and control mechanisms reduce errors and speed up issue resolution. When operations teams trust the system, scaling becomes an execution challenge, not a coordination problem.

Design compliant stablecoin payment infrastructure for global operations

What to Expect Next: A 2026 Stablecoin Payment Infrastructure Checklist

2026 stablecoin payment infrastructure checklist:

- Always-on settlement with clear transaction states and automated reconciliation across on-chain and off-chain systems.

- Native integration with card networks and enterprise payment workflows, including refunds, reporting, and settlement files.

- Transaction-level compliance controls enforced before value moves, covering identity, jurisdiction rules, and transfer limits.

- Multi-chain settlement support with routing based on cost, speed, and network reliability.

- Operational visibility designed for finance and payments teams, without requiring blockchain expertise.

- Support for sustained, high-frequency payment flows such as card spend, payouts, and treasury movements.

- Built-in auditability with complete, queryable transaction histories across systems.

Final Thoughts

Rain’s $1.95B valuation helps clarify where stablecoin payment infrastructure is actually headed. The market is rewarding systems built for real payment conditions, including regulatory scrutiny, operational load, and integration with existing financial rails, rather than products optimized for crypto native usage alone.

It also reflects a clear rise in stablecoin adoption within everyday payment flows. As these assets move into production environments, infrastructure quality matters more than novelty. Settlement reliability, reconciliation, and auditability are no longer future requirements. They are baseline expectations.

Taken together, this signals a shift in how stablecoin payments are viewed. They are no longer positioned as an emerging alternative, but as infrastructure increasingly embedded alongside cards, clearing systems, and treasury platforms. The teams building for this reality will set the pace.

Build Stablecoin Payment Solutions With Shamla Tech

Shamla Tech is a stablecoin development company building stablecoin payment platforms for enterprise use. We design systems that support compliant issuance, settlement, and reconciliation, aligned with real payment flows and regulatory requirements across global markets.

We build stablecoin infrastructure that scales with business operations, integrating stablecoins into existing payment rails, treasury workflows, and reporting systems. Our approach prioritizes reliability, auditability, and long term maintainability over experimental features or short term adoption metrics.