Stablecoins have moved beyond experimental digital assets to become a core layer of modern financial infrastructure. According to the Stablecoin Industry Report, the global stablecoin market has crossed $250 billion in circulation, driven by accelerating institutional adoption across payments, treasury operations, and on-chain settlement. Importantly, this growth is no longer speculative; it is increasingly fueled by enterprises using stablecoins as operational liquidity instruments.

The report highlights a structural shift in usage, from peer-to-peer transfers to enterprise-grade financial workflows, including cross-border settlement, internal treasury movements, and platform-based payouts. As regulatory clarity improves across major markets and infrastructure matures, stablecoins are being treated as programmable cash, rather than crypto-native products.

Why Stablecoins Are Becoming Enterprise Infrastructure

Stablecoin Payments at Scale Are Forcing a New Settlement Layer

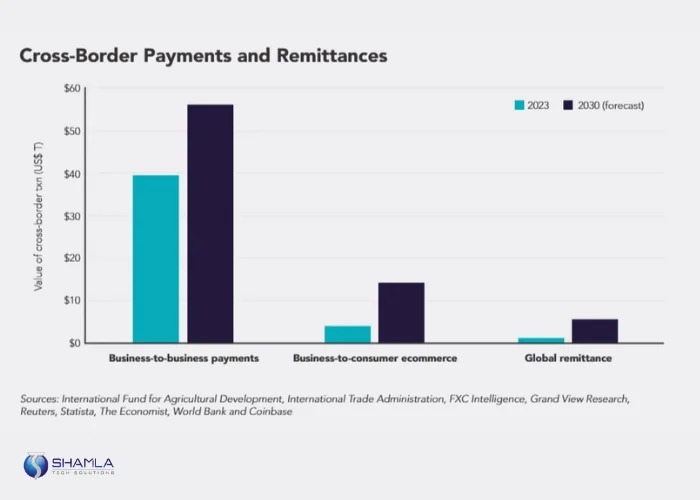

By the end of 2025, global cross-border payment flows are estimated to cross ~$45 trillion, driven mainly by business-to-business transactions such as supplier payments, intercompany transfers, and trade settlement.

As volumes rise, traditional banking rails struggle with cut-off times, multi-bank routing, and fee stacking. This scale pressure is pushing stablecoins into real payment flows, where value can move continuously, across borders, without waiting on banking windows or layered intermediaries.

Fragmented payment systems

Idle treasury capital

Settlement delays and FX loss

Limited liquidity visibility

Why enterprises are shifting

Stablecoins enable always-on settlement outside banking hours. Treasury teams gain direct control over cash movement across entities and regions. Funds can be deployed or settled within minutes.

By reducing dependence on intermediaries, enterprises simplify cash operations, lower transaction costs, and improve liquidity planning. Stablecoins are adopted as financial infrastructure because they solve operational problems at scale.

Types of Stablecoins

Stablecoin Type | Backing | Primary Use | Key Risk |

Fiat-backed stablecoins | Cash or cash equivalents | Payments, treasury movement, settlement | Reserve quality and redemption speed |

Crypto-backed stablecoins | Over-collateralized digital assets | On-chain applications | Price volatility and liquidation risk |

Algorithmic stablecoins | No reserves, rule-based supply | Experimental use only | Loss of price stability |

Commodity-backed stablecoins | Physical assets like gold | Hedging and asset exposure | Liquidity and pricing volatility |

1. Fiat-backed stablecoins

Fiat-backed stablecoins are issued against cash or short-term cash instruments held with regulated custodians. Each token represents a direct claim on real-world money. Value stability comes from full reserve backing and clear redemption rules.

These stablecoins are used for payments, treasury movement, and settlement flows. Key risks are reserve quality, custodian exposure, audit frequency, and how quickly holders can redeem under stress during extreme market disruption events and liquidity shocks.

2. Crypto-backed stablecoins

Crypto-backed stablecoins are supported by digital assets locked into smart contracts. To manage price swings, these systems require over-collateralization, meaning more value is locked than issued. Stability depends on automated liquidation rules and active market demand.

This structure introduces exposure to asset volatility, contract risk, and sudden liquidations. These models are mainly used within on-chain systems rather than for core cash or settlement operations in regulated financial environments today globally.

3. Algorithmic stablecoins

Algorithmic stablecoins attempt to hold price stability without asset reserves. Supply expands or contracts based on rules designed to influence market behavior. Value depends entirely on confidence, incentives, and continuous demand. When confidence breaks, price stability fails quickly.

These designs carry high structural risk, weak recovery paths, and limited regulatory acceptance, making them unsuitable for treasury, payments, or settlement use in large scale financial systems under stress conditions globally today.

4. Commodity-backed stablecoins

Commodity-backed stablecoins are linked to physical assets such as gold or other commodities. Token value follows the market price of the underlying asset. Reserves depend on physical custody, storage, and verification processes.

These stablecoins are used for asset exposure or hedging rather than daily payments. Risks include pricing volatility, lower liquidity, custody verification delays, and complex redemption tied to physical delivery across cross-border financial structures and settlement frameworks globally today.

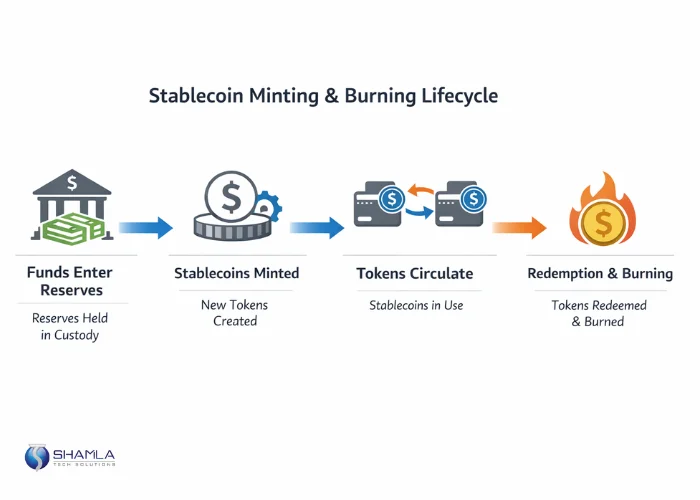

Stablecoin Minting/Burning Architecture

1. Funds enter reserves

2. Stablecoins are minted

3. Tokens circulate

4. Redemption triggers burning

Issuer and operator roles

Reserve custody model

On-chain and off-chain controls

Reserve Management & Treasury Controls

One-to-one backing principles

Custodian selection

Segregation of funds

Attestations and audits

Liquidity buffers

Technology and controls

Compliance Stack For Stablecoins

KYC and AML controls

Transaction monitoring

Sanctions screening

Reporting and audit trails

Governance workflows

Enterprise Stablecoin Use Cases

Treasury & Liquidity Management – Mercado Libre

Payments & Settlement – Visa

Platform & Ecosystem Payments – Stripe

Enterprise Deployment Models

1. Bank-Issued Model

In this model, a regulated bank issues and manages the stablecoin. Trust is high because reserves sit within the traditional banking system and controls follow existing financial standards. Settlement integrates cleanly with bank-led payment rails.

The trade-off is speed and flexibility. Product changes move slowly, integration options are limited, and customization is minimal. Access is often restricted to select clients, making this model less suited for dynamic payment flows or platform-led use cases.

2. Enterprise-Issued Model

Here, a company issues and operates its own stablecoin. This offers full control over minting, redemption rules, reserve structure, and integrations. Treasury logic, settlement flows, and user access can be tightly aligned to internal systems.

The cost is heavy regulatory and operational load. Compliance, reporting, audits, custody relationships, and risk controls must be built and maintained in-house. Scaling across regions increases complexity fast, especially where rules differ. This model suits organizations with strong compliance capacity and long timelines.

3. Platform-Enabled Model

In the platform-enabled model, issuance and operations are delivered through a specialized stablecoin infrastructure provider. Compliance, monitoring, reserve workflows, and reporting are modular and configurable. Businesses retain control over flows and use cases without owning the full regulatory stack.

This approach shortens launch timelines, supports multi-region deployment, and adapts as regulations change. Technical components such as minting logic, transaction screening, reconciliation, and audit trails are integrated by design. The same setup scales from B2B settlement to consumer-facing payments without re-architecture.

Build Your Stablecoin with Shamla Tech

Stablecoins are no longer experimental tools. They are becoming core financial infrastructure used for payments, treasury movement, settlement, and platform economics. Success depends on correct architecture, strong reserve controls, embedded compliance, and a deployment model that can scale across regions.

Shamla Tech is a stablecoin development company focused on building production-grade stablecoin infrastructure. The team designs minting and burning systems, reserve workflows, compliance layers, and integration frameworks that align with real-world financial operations.

Every implementation is built for auditability, liquidity control, and jurisdiction-aware deployment. From fiat-backed issuance to platform-enabled models, Shamla Tech helps organizations launch stablecoins that are secure, compliant, and ready to operate at scale.

Ready to modernize payments with stablecoins?

Contact us today to explore a platform that simplifies compliance, accelerates liquidity, and scales seamlessly across regions.